In November 2025, the average house price across the London Borough of Bexley held at £411,000 — and for owner-occupiers in Sidcup's DA14 and DA15 postcodes, that figure deserves a second look (ONS / HM Land Registry, Nov 2025). While the wider London average slipped 1.2% over the same twelve months, Bexley held firm. The equity in these homes didn't evaporate. It sat there — while the kitchen stayed too small and the third bedroom stayed a box room.

A single-storey extension in South East London runs £35,000–£90,000 in 2026. That's not a figure most DA14 families will find sitting in a savings account. So the question for Sidcup homeowners isn't really "can I extend?" — it's "which finance route costs me least, and when do I start?"

Related guide: How much a home extension costs in Sidcup

This guide unpacks every credible option: remortgage, further advance, second-charge mortgage, and personal loan. It maps each route to the property types that actually define Sidcup — from 1930s semis on Faraday Avenue in DA14 to the larger interwar detached homes tucked behind Foots Cray Meadows — and it's honest about which route costs less depending on where your mortgage currently sits.

TL;DR:

A single-storey extension in Sidcup costs £35,000–£90,000 in 2026. With Bexley house prices averaging £411,000 (ONS, Nov 2025) — steady while London fell — most DA14 and DA15 homeowners hold enough equity to fund one. A 5-year fixed remortgage at 4.25–4.50% typically beats a personal loan by thousands. Mid-deal on a low rate? A further advance or second-charge mortgage often works out cheaper.

Why Are Sidcup Homeowners Choosing to Extend Rather Than Move?

Moving has become a punishing transaction. Stamp duty on a £525,000 Sidcup purchase now costs £13,750. Layer on estate agent fees (£8,000–£13,000), conveyancing (£2,000–£4,000), and removals, and you're burning through £25,000–£35,000 before you've booked a plumber. And that's before you've dealt with a chain.

An extension costs a comparable amount — but it builds equity rather than spending it. Extensions across South East London typically return £1.20–£1.50 for every £1 spent, adding 10–20% to property value (RICS, 2025). On a £411,000 Sidcup home, that's £41,100–£82,200 in added value once the build is done.

The psychology has shifted too. Around 24% of UK homeowners who seriously considered moving in early 2026 chose to extend instead, citing disruption and transaction costs as the deciding factors (Quick Move Now, Q1 2026). In Sidcup, you can see it in planning portals: rear extension applications in DA14 and DA15 have grown steadily since 2023, particularly along Longlands Road and the streets off Rowanwood Avenue.

Cormac Hegarty, Director at Buildaway: "Sidcup homeowners come to us having already done the maths. The stamp duty alone on a like-for-like move in DA15 can wipe out a year's worth of mortgage overpayments. Extending a 1930s semi to add a proper kitchen-diner isn't just about space — it's often the financially smarter call by a significant margin."

Bexley's property market adds an important layer here: average prices rose 1.0% year-on-year to November 2025 while the wider London average fell 1.2% over the same period (ONS, Nov 2025). Sidcup homeowners are holding equity when equivalent mortgagors in other parts of the capital are watching theirs shrink.

🔑 Citation capsule: A well-executed home extension in South East London typically returns £1.20–£1.50 for every £1 spent and adds 10–20% to property value, according to the Royal Institution of Chartered Surveyors (RICS, 2025). For the average Sidcup homeowner — with Bexley borough prices at £411,000 (ONS, November 2025) — this translates to £41,100–£82,200 in added equity, comfortably ahead of financing costs for most projects.

How Much Does a Home Extension Actually Cost in Sidcup in 2026?

Knowing your realistic budget before approaching any lender matters more than people realise. Underestimate by £15,000 mid-project and you're forced into expensive short-term bridging — which erodes the return you were counting on.

Costs in London and the South East run 20–40% above the national average. In 2026, single-storey extensions in our area cost £2,800–£4,500 per m², compared to £2,000–£2,800 nationally (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A typical 20m² rear extension on a Sidcup semi — the kind that turns a galley kitchen into a proper open-plan space — realistically runs £56,000–£90,000 by the time you include professional fees, building control, and a 10–15% contingency.

Sidcup's interwar housing stock brings a specific consideration: most DA14 and DA15 properties sit on more generous plots than inner London terraces, which makes wraparound and side-return extensions genuinely viable — but the extra square footage tends to push costs higher. For period terraces closer to Sidcup High Street, a party wall surveyor is often necessary too; budget £1,000–£2,500 per adjoining property.

The approval picture in Bexley is encouraging. The London Borough of Bexley granted 88.4% of householder planning applications in recent reporting periods (BILTD, April 2026) — above the England average of 87%. Extensions get approved here. The process is rarely the obstacle; it's usually the funding.

Related guide: Single vs Double Storey Extension Guide for Sidcup

🔑 Citation capsule: In London and the South East, single-storey home extensions cost £2,800–£4,500 per m² in 2026 — 20–40% above the UK national average. A typical 20m² rear extension for a Sidcup DA14 or DA15 property therefore runs £56,000–£90,000 in total project cost, including professional fees and contingency (RICS BCIS, 2025; getestimateai.co.uk, March 2026).

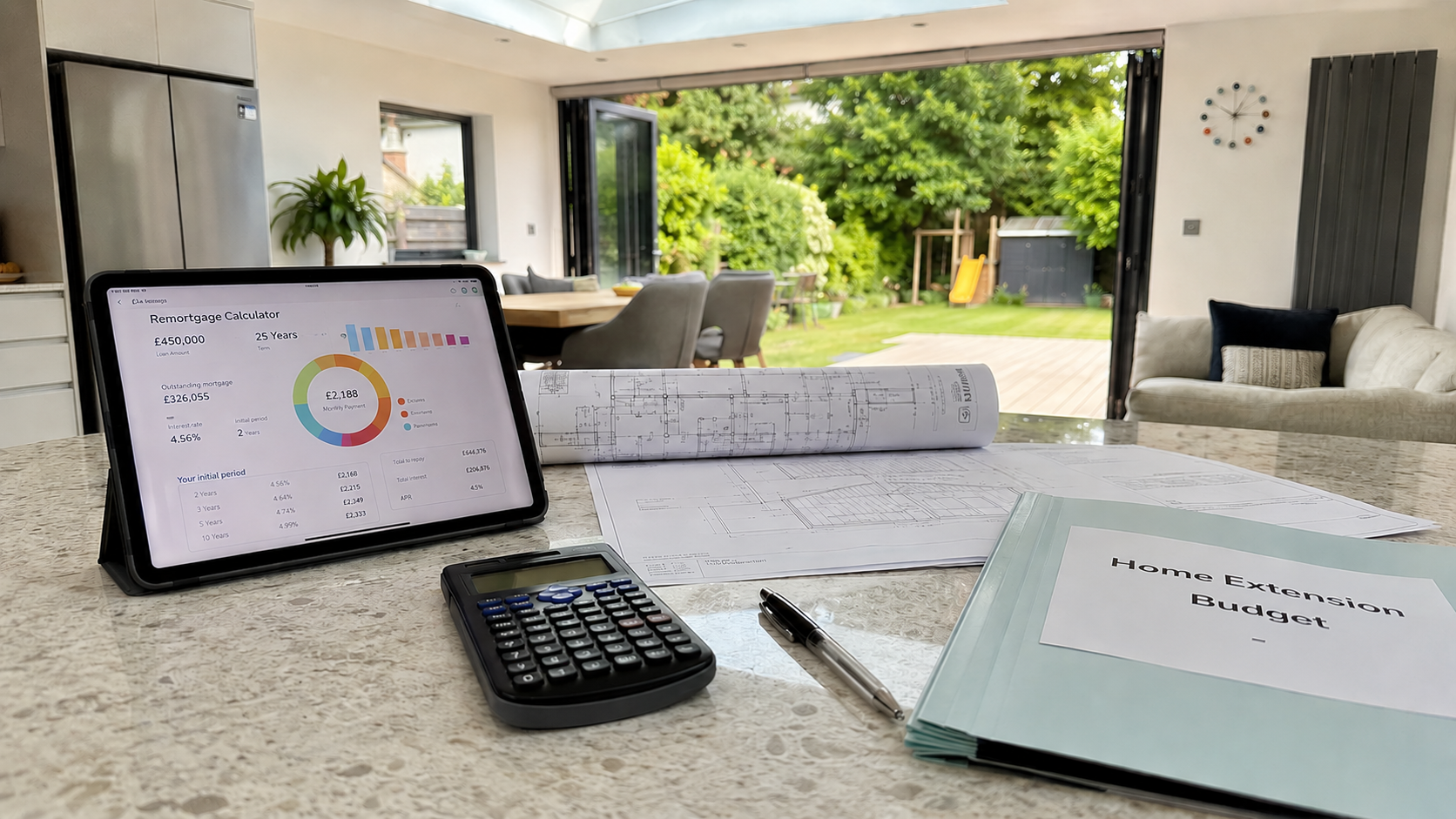

Should You Remortgage to Fund Your Sidcup Home Extension?

For homeowners whose current fixed deal is ending — or who've already drifted onto their lender's Standard Variable Rate — remortgaging is very often the most cost-effective way to fund an extension. The mechanism is straightforward: you replace your existing mortgage with a larger one, and the difference between the old balance and the new one comes to you as cash to fund the build.

In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Even at 75% LTV, the deals remain materially cheaper than any unsecured borrowing option available to homeowners.

When does remortgaging make most sense?

Timing is everything. Around 1.8 million fixed-rate mortgages are due to expire in 2026, many of them locked in at sub-2% rates in 2021 (UK Finance). If you're one of those homeowners, your deal is ending regardless. Remortgaging now lets you roll extension funding into a new competitive deal in a single move — rather than separately arranging a loan down the line.

If you stay put and do nothing, your lender's Standard Variable Rate currently averages 6.49–7.00% (HomeOwners Alliance, May 2026). On a £250,000 outstanding balance, the jump from 1.8% SVR adds over £1,100 per month. Remortgaging to 4.25% and pulling out £60,000 for the extension can cost almost the same monthly as drifting onto SVR and doing nothing at all — with a new kitchen at the end of it.

Watch out for Early Repayment Charges

If you're still mid-deal, you'll need to crunch the ERC numbers before committing. A homeowner paying a £5,000 ERC to remortgage and save £150 per month doesn't break even for nearly three years. In those cases, a further advance or second-charge mortgage is almost always the smarter route — details on both below.

💡 Our finding: Bexley's property market has consistently outperformed the wider London average on price stability. In the 12 months to November 2025, Bexley prices rose 1.0% while London as a whole fell 1.2% (ONS, Nov 2025). That divergence means Sidcup homeowners typically hold stronger LTV positions — and access better remortgage rates — than the London headline numbers might suggest.

The 6-month rule you need to know: You can lock in a new remortgage rate up to six months before your current fixed deal ends — with no ERC and no obligation to switch early. If your fix expires before November 2026, right now is the window to act.

Related guide: Planning Permission for a Sidcup Home Extension

🔑 Citation capsule: In May 2026, competitive 5-year fixed remortgage rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). UK Finance estimates 1.8 million fixed-rate mortgages will expire in 2026 — many held by homeowners who fixed below 2% — making this the primary window for Sidcup homeowners to remortgage for extension funding.

What Is a Further Advance — and Is It Right for Your Sidcup Property?

A further advance is borrowing additional money from your existing lender — layered on top of your current mortgage deal, without breaking or replacing it. It's probably the most underused finance option in this space, and for a specific group of Sidcup homeowners it's genuinely the best move available.

The appeal is simple: if you're sitting on a 1.8% fix that runs to 2027 or 2028, remortgaging means giving it up. A further advance lets you keep that rate on your existing balance while borrowing additional funds at today's market rates. Your original mortgage stays completely intact; the lender simply adds a second loan secured against the same property.

In practical terms: approval tends to move faster than a full remortgage — typically 2–4 weeks — because you're already a known customer with an established repayment record. The application is lighter too. The rate on a further advance is usually higher than your existing deal but considerably cheaper than any unsecured alternative.

The one caveat: not every lender offers further advances, and those that do may cap the available amount. If your lender doesn't offer one, or their rate isn't competitive, a second-charge mortgage (covered next) achieves exactly the same outcome without touching your main deal.

🏡 Buildaway tip: Homeowners in the Longlands and Blackfen areas of DA15 — particularly along Rowanwood Avenue and Longlands Road — often hold lower LTV ratios because larger interwar semis have appreciated strongly over the past decade. That lower LTV typically unlocks the most competitive further advance rates from mainstream lenders, making this option especially worth pursuing for DA15 owners before approaching alternative finance providers.

One practical rule for any finance route: get a written decision in principle before committing to a build timeline. Good Sidcup builders are booking weeks ahead — locking in finance before you sign contracts keeps your project on schedule and protects your deposit.

Related guide: How long a home extension takes in Sidcup

Option 3: Secured Loan (Second-Charge Mortgage) — When It Makes Sense in Sidcup

A second-charge mortgage is a separate loan secured against your property — sitting behind your primary mortgage in priority but drawing on the same asset as collateral. It's the right tool when breaking your existing mortgage deal would cost more than it saves.

Rates in 2026 typically run 4.5–7% depending on your LTV and credit profile (Fox Davidson, Jan 2026; ResiQuote, April 2026). That's higher than the best remortgage deals — but the trade-off is that your existing mortgage doesn't move. Your rate, your term, your monthly payment on the primary loan: all unchanged. Combined LTV across both loans usually can't exceed 75–85% with mainstream lenders.

This route suits you if:

- You're locked into a low fixed rate with an ERC still to run

- You're self-employed or contracting, and specialist second-charge lenders will assess your income more flexibly

- Your financial profile has changed since your original mortgage was agreed

- You need funds released faster than a full remortgage process allows

Sidcup's commuter profile — with strong representation in financial services, healthcare (Queen Mary's Hospital is a major local employer), and professional contracting — means a meaningful proportion of DA14 and DA15 homeowners are self-employed. Second-charge lenders often underwrite income differently from high-street remortgage products, and that flexibility has real value here.

One thing worth stating clearly: your property is collateral on both loans simultaneously. That's not a reason to avoid the route — it's a reason to model the combined repayments carefully before signing anything.

🔑 Citation capsule: A second-charge mortgage — also called a secured loan — sits behind your existing mortgage and allows Sidcup homeowners to borrow against property equity at rates of 4.5–7% in 2026, without disturbing their current mortgage deal. Combined LTV across both loans typically cannot exceed 75–85% (Fox Davidson, January 2026; ResiQuote, April 2026).

When Does a Personal Loan Make Sense for a Sidcup Extension?

A personal loan is the quickest path to extension finance — no equity calculation, no property valuation, no solicitor involvement. For certain projects, that speed and simplicity genuinely wins. But the numbers only stack up at the lower end of the cost range.

In 2026, personal loan rates run 6–10% for borrowers with solid credit histories, with the sharpest rates available on amounts between £7,500–£25,000 (ResiQuote, April 2026). Repayment terms cap out at 7 years, meaning monthly payments are noticeably higher than a mortgage-based route stretched over two decades.

To illustrate: £20,000 over 5 years at 7.5% costs roughly £401 per month, with total repayments around £24,060 — you pay £4,060 in interest. Compare that against the same sum added to a remortgage at 4.25% over 20 years, and the monthly cost drops significantly, though you pay more total interest due to the longer term.

For a smaller utility or garden room extension in DA14 — budget around £15,000–£20,000 — a personal loan is clean, fast, and avoids the administration overhead of remortgaging. It's also the right call when you simply want to keep your property equity entirely separate from your renovation decision.

Where it doesn't work: for most Sidcup extensions. Single-storey rear extensions here run £56,000–£90,000. At that scale, a secured route almost always wins on total cost.

Which Finance Route Fits Your Sidcup Property — by Postcode?

The right financing route depends on your property type and precise postcode as much as it does on your credit score. A DA14 terrace close to Sidcup Station and a DA15 interwar detached backing onto Foots Cray Meadows present very different equity profiles — and call for different approaches.

📊 Buildaway equity snapshot — Sidcup postcodes: Based on HM Land Registry and ONS data (November 2025–May 2026), here's how much a homeowner at 75% LTV could typically unlock, assuming a 50% LTV outstanding mortgage:

| Property Type | Area | Avg Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| 1930s semi-detached | DA14 (Faraday Ave, Camborne Rd) | £380k–£500k | £95k–£125k | Remortgage or Further Advance |

| Interwar semi / larger detached | DA15 (Longlands, Blackfen) | £420k–£580k | £105k–£145k | Further Advance or Remortgage |

| Period terrace | DA14 (Sidcup High St area) | £340k–£460k | £85k–£115k | Second Charge (if mid-fix) |

| Detached / conservation area | DA14 (Foots Cray, North Cray Rd) | £500k–£750k+ | £125k–£187k | Any route; remortgage most flexible |

| Smaller flat / maisonette | DA14 (central Sidcup) | From £250k | From £62k | Personal loan for smaller projects |

*Assumes 50% LTV outstanding balance; figures indicative only. Always seek independent mortgage advice.

Foots Cray and Old Bexley — a special planning note. Properties in Bexley's 31 conservation areas — including Foots Cray and Old Bexley — often achieve premium valuations that unlock generous equity headroom. The trade-off: some lenders require full planning permission before releasing funds in conservation areas, because heritage design restrictions affect build viability and therefore the security value for the lender. If you're in one of these areas, start your planning conversation with Bexley Council before approaching any lender.

🔑 Citation capsule: The right financing route for a Sidcup home extension depends on both property type and postcode. Homeowners in DA15 — where larger interwar semis in Blackfen and Longlands command values of £420,000–£580,000 (HM Land Registry, Nov 2025) — typically hold the strongest equity positions and qualify for the most competitive further advance and remortgage rates in the Bexley area.