Lewisham is one of South East London's most actively extending boroughs — and in 2026, the financial case for staying and building has rarely been stronger. Terraced houses in SE13 now average £798,800, up 5% year-on-year, while the borough's transport connectivity and the anticipated Bakerloo line extension continue to underpin long-term confidence across SE13, SE4, and SE6 (Rightmove / HM Land Registry, 2026; ONS, Feb 2026).

A rear kitchen extension or side return on a Victorian terrace in Hither Green or a 1930s semi near Ladywell will realistically cost £50,000–£100,000 in 2026. Most families don't have that in a current account. The decision isn't whether to extend — for most Lewisham homeowners it's the obvious choice over moving. It's which finance route costs you least and fits your specific mortgage position.

Related guide: How much a home extension costs in Lewisham

This guide maps every option — remortgage, further advance, second-charge mortgage, and personal loan — against the specific property types found across SE13, SE4, and SE6. Whether you own a Victorian terrace on the Corbett Estate in Hither Green, an Edwardian semi near Manor House Gardens, or a 1930s house in Brockley or Catford, the right finance route isn't the same for every homeowner.

TL;DR:

SE13 terraced homes average £798,800 in 2026 — up 5% year-on-year (Rightmove / HM Land Registry). Semi-detached properties in SE13 reach £1,087,120. Most SE13, SE4, and SE6 homeowners who've owned for five or more years hold meaningful equity, often at LTV ratios well below 60%. Remortgaging at 5-year fixed rates of 4.25–4.50% is the most cost-effective route when your deal is ending. Mid-fix with a good rate? A further advance or second-charge mortgage almost always makes more sense. Lewisham's multiple conservation areas — Ladywell, Lee Manor, Brockley, Telegraph Hill — can affect lender pre-planning conditions and are worth understanding before you apply.

Why Are Lewisham Homeowners Choosing to Extend Rather Than Move?

Lewisham's property market has a quality that makes the extend-versus-move calculation particularly straightforward. The Victorian and Edwardian terraces around Hither Green Station (SE13), along St Swithun's Road, and across the Corbett Estate are the kind of homes buyers compete hard for. Once you're established in one, the case for leaving rarely stacks up — especially when the transaction costs of moving at this price point are examined honestly.

Stamp duty on an £850,000 Lewisham property now stands at £32,500 under 2026 HMRC rates. Add estate agent fees (£12,000–£21,000), conveyancing (£2,500–£5,000), and the renovation work that comes with most period properties, and relocating to gain a room or create an open-plan ground floor can consume £60,000–£90,000 before any value is built.

A home extension turns that same investment into a permanent capital improvement. Across South East London, extensions return £1.20–£1.50 for every £1 spent and add 10–20% to property value (RICS, 2025). On an SE13 terrace worth £799,000, a well-designed rear extension could add £79,900–£159,800 in equity — substantially more than the financing cost of any mortgage-backed project.

Cormac Hegarty, Director at Buildaway: "Lewisham is a borough where families have often invested for years — in the renovation, in the garden, in the schools catchment. The homeowners we work with here on Hither Green streets and around Ladywell aren't weighing up whether to stay. They're asking how to fund the extension they've already designed in their heads. That's exactly the conversation this guide is built around."

Around 24% of UK homeowners who seriously considered moving in early 2026 chose to extend instead (Quick Move Now, Q1 2026). In Lewisham — where Lewisham Station reaches London Bridge in 8 minutes by National Rail, Hither Green Station connects to London Bridge in 14 minutes, and the proposed Bakerloo line extension would add Tube connectivity to the borough — the long-term rationale for owning here is strengthening, not weakening.

🔑 Citation capsule: Home extensions in South East London typically return £1.20–£1.50 for every £1 spent, adding 10–20% to property value (RICS, 2025). For a Lewisham homeowner with an SE13 terraced property averaging £798,800 in 2026 (Rightmove / HM Land Registry) — up 5% year-on-year — this represents £79,880–£159,760 in potential added equity. Combined with 8-minute access to London Bridge and the borough's infrastructure pipeline, this makes a well-financed extension one of the most rational capital decisions in South East London.

How Much Does a Home Extension Actually Cost in Lewisham in 2026?

Before approaching any lender, you need a budget you can defend. In Lewisham, getting this wrong by £15,000–£20,000 — a figure easily absorbed by party wall agreements, conservation area requirements, or simply London's labour premium — is how homeowners end up mid-project without enough runway.

Across London and the South East, single-storey extensions cost £2,800–£4,500 per m² in 2026 — a 20–40% premium over national average rates (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A 20m² rear extension on a Victorian terrace in Hither Green (SE13 5) or a 1930s semi in Catford (SE6) realistically totals £58,000–£95,000 including building control, professional fees, and a properly costed contingency.

The conservation area factor. Lewisham has more designated conservation areas than most neighbouring boroughs — Ladywell, Lee Manor, Brockley, Telegraph Hill (SE4), Culverley Green (SE6), Brookmill Road (SE8), and multiple sectors of Blackheath (SE13) — each managed by the London Borough of Lewisham Planning Department at Laurence House, Catford Road (SE6 4RU). Properties within these zones must use materials consistent with the conservation area character appraisal. That often means matching original brick, heritage-specification windows, and a pre-application design discussion — costs that run £800–£2,500 before a planning application is even submitted.

Party wall agreements are a near-universal requirement for terraced properties across SE13 and SE4 — budget £1,000–£2,500 per neighbouring property. Planning fees start at £206 for a householder application; building control runs £400–£2,000.

The approval rate remains encouraging: 87% of householder applications in England were granted in the year ending September 2025 (DLUHC, Dec 2025). Lewisham's grant rates are described by planning specialists as above the national average for well-prepared applications.

Related guide: Single vs Double Storey Extension — Lewisham

🔑 Citation capsule: In London and the South East, single-storey home extensions cost £2,800–£4,500 per m² in 2026 — 20–40% above the UK national average (getestimateai.co.uk, March 2026; RICS BCIS, 2025). For Lewisham homeowners within one of the borough's multiple conservation areas — including Ladywell, Brockley, Lee Manor, and Telegraph Hill — heritage-compliant materials and pre-application design advice add a further £1,500–£4,500 to total project costs versus comparable non-designated properties in SE13 or SE6.

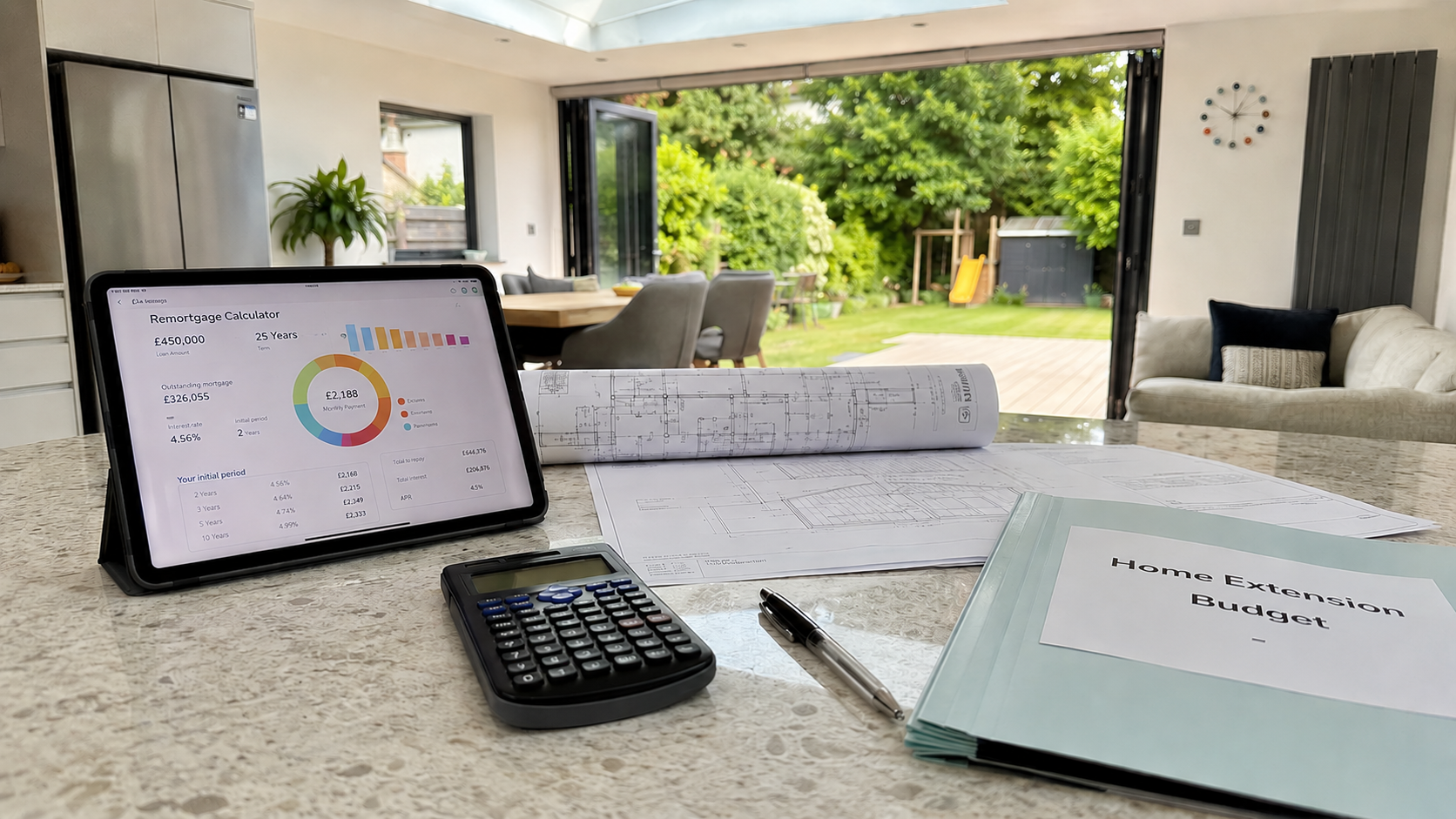

Should You Remortgage to Fund Your Lewisham Home Extension?

Remortgaging is the route most Lewisham homeowners land on — and when the timing aligns with your current deal, it consistently delivers the best overall cost outcome.

The structure is well understood: your existing mortgage is replaced by a new, larger one. The difference between your previous outstanding balance and the new amount arrives as cash for the build. In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Given that SE13 terraced homes average £798,800 — up 5% year-on-year — homeowners who bought five or more years ago frequently sit well below 50% LTV, qualifying them for the most competitive pricing tier in the market.

When does remortgaging suit a Lewisham homeowner?

It makes most sense when your current fixed deal is ending or has already expired. UK Finance estimates around 1.8 million fixed-rate mortgages will expire in 2026, many locked in below 2% in 2021. If your deal is one of them, remortgaging now allows you to lock in a new rate and release extension funding in one combined transaction — rather than managing two separate financial decisions.

The alternative is landing on your lender's Standard Variable Rate (SVR), currently averaging 6.49–7.00% (HomeOwners Alliance, May 2026). For a Lewisham homeowner with £290,000 outstanding, the monthly step-up from a 1.8% fix to SVR is substantial. Remortgaging at 4.25% and simultaneously releasing £65,000 for a rear extension can add only a fraction more each month compared to drifting onto SVR with nothing to show for it.

The Early Repayment Charge (ERC) calculation

Mid-deal homeowners need to model this carefully. Many SE13 homeowners who fixed at sub-2% in 2021 still carry ERCs of 1–5% on meaningful balances. On a £320,000 outstanding mortgage, a 3% ERC means £9,600 in exit costs. If remortgaging saves £350 per month, that ERC takes over 27 months to recover. In that scenario, a further advance from your existing lender almost always delivers the better financial result.

💡 Our finding: SE13 terraced prices rose 5% year-on-year to early 2026 (Rightmove / HM Land Registry) — one of the strongest growth rates in South East London at this price level. The anticipated Bakerloo line extension to Lewisham, flagged for potential TfL funding approval, is already being priced into local market sentiment. For homeowners on Hither Green streets like St Swithun's Road and along the Corbett Estate, equity has grown faster than many realise — and that LTV improvement directly translates into better remortgage pricing.

The 6-month rule. You can lock in a new remortgage rate up to 6 months before your current deal expires — at no cost and with no obligation to draw down early. If your fix ends before November 2026, the window is open now. Remortgaging activity grew 13.7% in 2025 to 1.86 million loans (UK Finance); specialist brokers familiar with Lewisham's conservation area planning context are worth the investment.

Related guide: Planning Permission for a Lewisham Home Extension

🔑 Citation capsule: In May 2026, the Bank of England base rate stands at 3.75%, with competitive 5-year fixed remortgage deals at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026; Bank of England, May 2026). SE13 terraced homes averaging £798,800 — up 5% year-on-year (Rightmove / HM Land Registry, 2026) — give long-term Lewisham owners access to LTV positions well below 50%, unlocking the most competitive remortgage pricing available in the market.

What Is a Further Advance — and Is It Right for Lewisham's Conservation Area Homeowners?

A further advance is additional money borrowed from your existing mortgage lender — on top of your current mortgage, without touching the original deal. No early repayment charge. Your existing rate stays exactly as it is.

For Lewisham homeowners in one of the borough's many conservation areas — Ladywell (SE13), Lee Manor (SE12), Brockley (SE4), Telegraph Hill (SE4), or Culverley Green (SE6) — the further advance has a specific operational advantage. A full remortgage sometimes triggers a lender's requirement to see planning approval before funds are released on conservation-designated properties. A further advance typically avoids this: since the lender is already holding your mortgage and has your property on file, the additional documentation burden around planning designation is usually simpler.

What to realistically expect:

Further advance rates sit slightly above your existing mortgage rate — lenders treat the incremental risk differently — but remain materially cheaper than personal borrowing. Applications typically resolve in 2–4 weeks, faster than a full remortgage, and since you're already in the lender's system with a verified payment history, the approval process is leaner.

Not all lenders offer further advances, and some cap the maximum facility. If yours doesn't, a second-charge mortgage achieves the same practical outcome: preserving your existing deal while releasing equity from your property.

🏡 Buildaway tip: Victorian terraces on the Corbett Estate in Hither Green (SE13 6) — one of the most intact Victorian planned estates in South South London — consistently attract strong valuations and above-average buyer demand. Homeowners here, and on streets like Kellerton Road (SE13 5RD) where a November 2025 sale reached £1,150,000, frequently hold LTV ratios below 40%. That equity position puts them firmly within the further advance pricing tier where lenders compete hard for business. Always get a formal decision in principle before committing to a build programme.

Related guide: How long a home extension takes in Lewisham

Option 3: Secured Loan (Second-Charge Mortgage) — Navigating Lewisham's Conservation Patchwork

A second-charge mortgage is a separate loan secured against your property, sitting behind your existing mortgage. It's the route that solves the specific financing problem that arises when your existing deal is worth keeping and your conservation-area lender applies a pre-planning condition on a full remortgage.

Lewisham's conservation area coverage is more extensive than most homeowners realise. Planning notices from the London Borough of Lewisham (Laurence House, Catford Road SE6 4RU) regularly cover Blackheath Conservation Area (SE13), Telegraph Hill (SE4), Brockley (SE4), Brookmill Road (SE8), Culverley Green (SE6), and Forest Hill (SE23) in a single weekly publication. If your property is within any of these zones, a mainstream remortgage lender may want planning confirmation before releasing funds — because conservation-area design restrictions can affect a project's viability and, in turn, the property's value as mortgage security.

Second-charge mortgages typically assess the property on its security value alone. That removes the pre-planning condition — giving you access to finance while architect drawings and planning discussions are still in progress.

Rates in 2026 run 4.5–7% depending on LTV and credit profile (Fox Davidson, Jan 2026; ResiQuote, April 2026). The combined LTV across both loans typically can't exceed 75–85% with mainstream second-charge lenders.

This route suits Lewisham homeowners who:

- Are mid-deal with a sub-2.5% rate and a meaningful ERC that makes remortgaging uneconomical

- Own a property within one of Lewisham's conservation zones and want access to funds before planning is granted

- Are self-employed, a contractor, or operate variable income — specialist second-charge lenders underwrite income more flexibly than high-street remortgage teams

- Need funds within 3–4 weeks rather than waiting for a full remortgage to complete

Your home secures both loans — this is a genuine risk and not one to understate. Get independent mortgage advice before proceeding.

🔑 Citation capsule: A second-charge mortgage allows Lewisham homeowners to borrow against their property equity at 4.5–7% in 2026 without disturbing their existing mortgage deal (Fox Davidson, January 2026; ResiQuote, April 2026). For properties within Lewisham's multiple conservation areas — Ladywell, Lee Manor, Brockley, Telegraph Hill, and Culverley Green — where mainstream lenders sometimes require planning approval before releasing remortgage funds, second-charge lenders typically provide a more flexible pre-planning finance route.

When Does a Personal Loan Make Sense for a Lewisham Extension?

A personal loan is the right tool for a specific type of Lewisham project — and wrong for most of them.

Personal loan rates in 2026 sit at 6–10% for borrowers with good credit, with the best deals on amounts between £7,500–£25,000 (ResiQuote, April 2026). Terms cap at 7 years, which pushes monthly payments higher than any mortgage-based route and makes the product uncompetitive on anything above £25,000 in project cost.

The maths: £25,000 over 5 years at 7% costs £495/month and totals £29,700 — meaning £4,700 in interest. For a compact garden room, a small utility extension, or a modest porch conversion on a Catford (SE6) terrace or a smaller flat in Ladywell — where project costs might land at £15,000–£22,000 — a personal loan is clean, fast, and leaves your property equity entirely untouched.

What it doesn't suit: the majority of Lewisham extensions. A rear kitchen-diner on a Victorian terrace in Hither Green or a side return on an Edwardian semi near Manor House Gardens will realistically cost £60,000–£100,000. At those sums, the rate differential between a personal loan and a remortgage or second-charge translates to thousands of pounds in additional interest over any reasonable repayment period. The financial case simply doesn't hold.

Which Finance Route Fits Your Lewisham Property — by Postcode and Type?

Lewisham's housing stock is more varied than people expect. The Victorian terraces of the Corbett Estate in Hither Green (SE13 6) sit at the premium end of the borough. Edwardian semis cluster around Manor House Gardens (SE12) and along the Lee borders. The 1930s stock extends through Brockley (SE4), Catford (SE6), and Bellingham. Newer builds and smaller flats occupy pockets throughout. Each type carries different equity characteristics and finance considerations.

📊 Buildaway equity calculator — Lewisham postcodes: Based on Rightmove and HM Land Registry data (2026), here is the approximate additional borrowing available at 75% LTV for Lewisham homeowners, assuming a 45% LTV outstanding mortgage:

| Property Type | Area | Approx Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Victorian terrace (Corbett Estate) | SE13 6 (Hither Green, St Swithun's Rd) | £650k–£1.15m | £182k–£375k | Remortgage or Further Advance |

| Victorian/Edwardian terrace | SE13 5 (Lewisham, Ladywell borders) | £550k–£800k | £138k–£248k | Remortgage or Further Advance |

| 1930s semi-detached | SE4 (Brockley, Honor Oak borders) | £500k–£750k | £125k–£206k | Further Advance or Remortgage |

| Edwardian semi (conservation zone) | SE13 / SE12 (Lee Manor, Manor House Gardens) | £580k–£870k | £146k–£254k | Second Charge (if conservation pre-planning applies) |

| 1930s terrace / smaller | SE6 (Catford, Bellingham, Culverley Green) | £420k–£620k | £105k–£171k | Further Advance or Remortgage |

| Purpose-built flat | SE13 / SE6 (various) | From £300k | From £63k | Personal loan for smaller scope |

*Assumes 45% LTV outstanding; indicative only — always seek independent mortgage advice.

Lewisham's infrastructure story — and why it matters for equity. Unlike the other locations in this series, Lewisham has an infrastructure catalyst that actively reinforces its extend-not-move logic. The proposed Bakerloo line extension to Lewisham — flagged by TfL for potential funding approval and described by the Deputy Mayor for Transport as having the 'planets align' in 2025 — would bring Tube connectivity directly to SE13 (Lewisham London). A second phase could integrate Ladywell and Catford Bridge stations into the Underground network. That prospect, even at planning stage, supports property values and strengthens the investment thesis for extending rather than selling.

Lewisham's grant rates for householder extensions are above the national average when applications are well-prepared, according to planning specialists (Rubix Planning, 2026). The borough is described as one that supports intensification in accessible locations — a planning culture that works in the homeowner's favour.

Related guide: Planning Permission for a Lewisham Home Extension

🔑 Citation capsule: Lewisham's SE13 terraced homes average £798,800 in 2026 — up 5% year-on-year (Rightmove / HM Land Registry). Semi-detached properties in SE13 reach £1,087,120. Long-term owners on the Corbett Estate in Hither Green, with properties valued at £650,000–£1.15m, frequently hold LTV ratios well below 40%, unlocking the most competitive remortgage and further advance rates available. The anticipated Bakerloo line extension to Lewisham reinforces the borough's infrastructure fundamentals and long-term equity outlook.