In early 2026, the average house price across SE15 Peckham reached £455,000 - and for homeowners along Bellenden Road, Choumert Road, and the streets surrounding Peckham Rye, that figure represents substantial equity sitting untapped while growing families squeeze into rooms that no longer fit their lives (HM Land Registry, Feb 2026).

A single-storey rear extension in South East London now runs £35,000–£90,000. That's not spare cash most families can pull from savings. So the real question isn't "can I afford to extend?" - it's "which finance route costs the least, and when do I pull the trigger?"

Related guide: How much a home extension costs in Peckham

This guide walks through every route available: remortgage, further advance, second-charge mortgage, and personal loan. Crucially, it maps each option to the specific property types and pricing realities found across Peckham's postcodes - from Victorian terraces on Choumert Grove in SE15 to the larger period homes along Friern Road in SE22 East Dulwich.

TL;DR:

A single-storey extension in Peckham costs £35,000–£90,000 in 2026. With average SE15 prices at £455,000 (HM Land Registry, Feb 2026), most homeowners hold enough equity to fund one without selling. Remortgaging at today's 5-year fixed rates of 4.25–4.50% typically beats personal borrowing by thousands. If you're locked into a low rate mid-deal, a further advance or second-charge mortgage almost always works out cheaper.

Why Are Peckham Homeowners Choosing to Extend Rather Than Move?

The financial case for staying put has never been stronger - and the numbers tell the story clearly. Stamp duty on a £600,000 Peckham property now costs £22,500. Add estate agent fees of £9,000–£15,000, conveyancing costs of £2,000–£4,000, and removals, and you're spending £35,000–£45,000 just to land somewhere else - before you've opened a single box.

A well-planned extension costs a similar amount but produces the opposite outcome: it builds value rather than burning it. Extensions across South East London consistently return £1.20–£1.50 for every £1 spent, adding 10–20% to a property's value (RICS, 2025). On a £455,000 Peckham home, that's £45,500–£91,000 in added equity.

It's not purely financial either. Around 24% of UK homeowners who seriously considered moving in early 2026 ultimately chose to extend instead, citing the cost of moving and the disruption to schooling and community as primary drivers (Quick Move Now, Q1 2026). In SE15, where Bellenden Village has become one of South London's most sought-after pockets and school catchments are fiercely competitive, that figure feels intuitive. People don't want to leave - they want more space where they already are.

Cormac Hegarty, Director at Buildaway: "The clients we work with in Peckham and East Dulwich have usually already done the maths before they call us. Moving means losing the street, the school, the community. So the conversation goes straight past 'should I extend?' and lands immediately on 'how do I fund it?' - which is exactly what this guide addresses."

Peckham's market has its own particular character: SE15 properties have held value steadily as creative and professional demand has reshaped the area over the past decade. Equity that was modest five years ago is now substantial - and it's sitting unused in a lot of three-bedroom terraces along Nunhead Lane and Maxted Road.

🔑 Citation capsule: A well-executed home extension in South East London typically returns £1.20–£1.50 for every £1 spent and adds 10–20% to property value, according to the Royal Institution of Chartered Surveyors (RICS, 2025). For the average SE15 Peckham homeowner at £455,000, that means between £45,500 and £91,000 in added equity - a return that comfortably absorbs the cost of financing for most projects.

How Much Does a Home Extension Actually Cost in Peckham in 2026?

Before any lender conversation happens, you need a grounded budget. London and South East build costs run 20–40% above the national average - and Peckham's inner-London location places it firmly at the top of that band.

In 2026, single-storey extensions here cost £2,800–£4,500 per m², against a UK national average of £2,000–£2,800 (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A typical 20m² rear extension on a SE15 Victorian terrace - with structural work, bi-fold doors, and a proper kitchen fit-out - realistically lands at £56,000–£90,000 once you include professional fees, building control, and a 10–15% contingency.

There are add-on costs specific to Peckham's housing stock that catch many homeowners out. Victorian terrace owners on streets like Talfourd Road or Lyndhurst Way will almost certainly need a party wall surveyor - budget £1,000–£2,500 per affected neighbour. Planning fees for a standard householder application start at £206. Building control typically adds £400–£2,000 depending on project scope. Properties within the Holly Grove or Glengall Road Conservation Areas may face additional heritage design requirements that push architect fees noticeably higher.

The upside: 87% of householder planning applications in England were approved in the year ending September 2025 (DLUHC, Dec 2025). Extensions that are well-designed and sympathetically detailed get through.

Knowing your all-in project cost before approaching any lender isn't optional - it's the difference between a smooth process and an expensive mid-build scramble for emergency funds.

Related guide: Single vs Double Storey Extension Guide

🔑 Citation capsule: In London and the South East, single-storey home extensions cost £2,800–£4,500 per m² in 2026 - running 20–40% above the UK national average. A typical 20m² rear extension on a Peckham Victorian terrace therefore totals £56,000–£90,000 in full project cost, including professional fees, building control, and contingency (RICS BCIS, 2025; getestimateai.co.uk, March 2026).

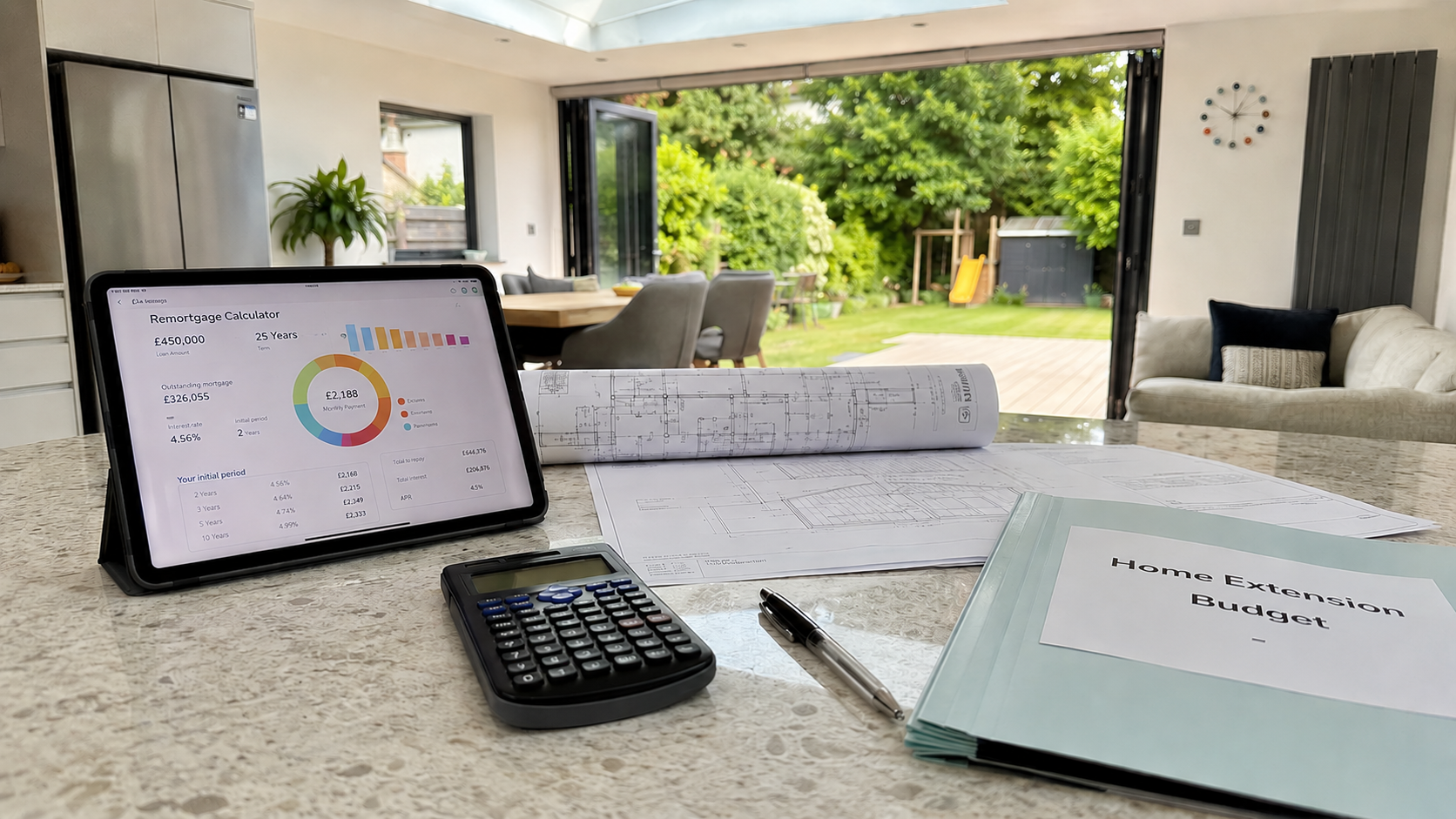

Should You Remortgage to Fund Your Peckham Home Extension?

For many SE15 and SE22 homeowners, remortgaging is the first option they consider - and when the timing lines up, it's hard to beat on overall cost.

The mechanics are straightforward: your existing mortgage is replaced with a larger one, and the difference between your old balance and the new loan amount is released as cash to fund the build. In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Even at 75% LTV, secured borrowing remains far cheaper than any form of unsecured personal credit.

When does remortgaging work best for Peckham homeowners?

The strongest scenario is a deal that's expiring or has already rolled off. Around 1.8 million fixed-rate mortgages are due to expire in 2026 across the UK, many of them locked in at sub-2% in 2021 (UK Finance). If you're one of those homeowners, your rate is ending regardless. Remortgaging now lets you move to a new deal and release extension funding simultaneously - one application, two problems solved.

The alternative is doing nothing and drifting onto your lender's Standard Variable Rate (SVR), which currently averages 6.49–7.00% (HomeOwners Alliance, May 2026). On a £280,000 outstanding mortgage, that's roughly £1,400 extra per month compared to a 4.25% fix. Remortgaging at a competitive rate and releasing £60,000 for an extension can cost almost the same monthly as drifting onto SVR and doing nothing at all.

Watch out for Early Repayment Charges

If you're mid-deal, you'll need to weigh the ERC against the interest saving. ERCs of 1–5% of the outstanding loan balance are common on 2021-era mortgages. Paying a £5,500 ERC to switch to a rate that saves you £180 per month takes 30 months to break even - by which point your current deal would likely have ended anyway. A further advance or second-charge mortgage is frequently the smarter path in this situation.

💡 Our finding: SE15 has seen sustained interest from buyers seeking well-connected inner-London living at a relative discount to other South London postcodes. That demand has kept values resilient - meaning Peckham homeowners are sitting on meaningfully more equity than buyers who entered the market more recently elsewhere in the capital. Stronger equity means better LTV positions and access to the most competitive remortgage tiers.

The 6-month rule: You can lock in a new remortgage rate up to 6 months before your current deal expires, with no ERC and no obligation to complete early. If your fix ends before November 2026, the optimal window to apply is now.

Remortgaging activity grew 13.7% in 2025 to 1.86 million refinancing loans (UK Finance). Brokers who specialise in South London properties understand the local valuation picture - worth the cost.

Related guide: Planning Permission for a Peckham Home Extension

🔑 Citation capsule: In May 2026, competitive 5-year fixed remortgage rates stand at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). UK Finance projects 1.8 million fixed-rate mortgages will expire in 2026, most held by homeowners who locked in below 2% in 2021. For Peckham homeowners on expiring deals, this creates a direct window to remortgage and release extension funding at the same time.

What Is a Further Advance - and Is It Right for Your Situation?

A further advance is borrowing additional money directly from your existing mortgage lender, on top of your current deal, without triggering a break or an Early Repayment Charge. It's the option that gets overlooked most often - and for a significant portion of SE15 homeowners, it's the most cost-effective move available.

Here's the core appeal: if you fixed at 1.8% in 2021 and that deal runs until 2027, remortgaging means surrendering that rate. A further advance lets you keep it entirely intact. Your lender adds a second tranche of borrowing - secured on the same property - at a current market rate, while your original mortgage continues exactly as agreed.

What to expect from the process:

The rate applied to a further advance will typically sit above your existing mortgage rate, but well below what you'd pay on a personal loan. Processing times tend to be faster than a full remortgage - some lenders turn these around in 2–4 weeks. The application is also considerably lighter, since you're an existing customer with an established track record.

The limitation: not every lender offers this product, and some cap the available amount. If your current lender doesn't provide a further advance at a competitive rate, a second-charge mortgage achieves the same structural outcome without disturbing your main deal.

🏡 Buildaway tip: Homeowners in SE22 East Dulwich - particularly along Friern Road, Upland Road, and the streets near Dulwich Park - often hold lower LTV ratios than equivalent SE15 addresses, thanks to the area's higher average values (£700,000–£900,000+ for four-bedroom semis, per HM Land Registry, April 2026). That equity cushion typically unlocks the most attractive further advance rates from mainstream lenders.

Get a written decision in principle before committing to any build timeline. Reputable contractors in the SE15 and SE22 area book weeks in advance - confirmed finance should precede any contract signature.

Related guide: How long a home extension takes in Peckham

Option 3: Secured Loan (Second-Charge Mortgage) - When It Makes Sense

A second-charge mortgage places a separate loan against your property, sitting behind your existing mortgage in priority order but using the same asset as security. It's not a first-resort option, but it's the right tool for a specific and common set of circumstances.

In 2026, rates on second-charge products generally run 4.5–7%, depending on your LTV, credit profile, and lender (Fox Davidson, Jan 2026; ResiQuote, April 2026). That's higher than the best remortgage deals, but the crucial trade-off is clear: your first mortgage stays exactly as negotiated. Combined LTV across both loans typically can't exceed 75–85% with mainstream lenders.

This route makes sense if:

- You're mid-deal on a rate worth preserving and the ERC is material

- You're self-employed, a contractor, or have non-standard income that specialist lenders assess more flexibly than high-street remortgage underwriting

- Your project timeline requires faster access to funds than a full remortgage permits

- Your income structure has changed materially since your original application

Peckham and East Dulwich have attracted a significant proportion of freelancers, creative industry professionals, and tech contractors over the past decade. For these homeowners, second-charge lenders often offer income assessment models that suit portfolio or variable earnings far better than standard remortgage underwriting.

One honest note: both your mortgage and the second charge are secured against your home. If either becomes unserviceable, both are at risk. This isn't a reason to avoid the product - it's a reason to ensure the numbers work before you commit.

🔑 Citation capsule: A second-charge mortgage allows Peckham homeowners to borrow against their property equity at rates of 4.5–7% in 2026, without affecting their existing mortgage deal. The combined LTV across both loans typically cannot exceed 75–85% with mainstream lenders, making available equity the primary constraint (Fox Davidson, January 2026; ResiQuote, April 2026).

When Does a Personal Loan Make Sense for a Peckham Extension?

A personal loan is the cleanest, fastest route to extension finance - no valuation, no solicitor, no impact on your mortgage. But it only pencils out economically at the lower end of project budgets.

In 2026, personal loan rates run 6–10% for applicants with strong credit histories, with the sharpest rates available on borrowing between £7,500–£25,000 (ResiQuote, April 2026). Maximum terms are capped at 7 years, which pushes monthly repayments higher than a mortgage product spread over 20–25 years.

To illustrate: £25,000 over 5 years at 7% costs roughly £495 per month, with total repayments of £29,700 - meaning £4,700 in interest paid. The same sum remortgaged at 4.25% across a 20-year term carries a lower monthly payment, though total interest rises with the extended repayment period.

When a personal loan is the right call for a Peckham homeowner:

A compact rear infill or utility addition on a Nunhead terrace - budget £15,000–£20,000 - is a sensible personal loan candidate. It's fast, uncomplicated, and keeps your property equity entirely separate from the renovation decision. Some homeowners genuinely prefer this separation.

What it won't work for: the majority of Peckham extensions. Full rear single-storey projects in SE15 run £56,000–£90,000. At that budget level, secured finance wins on cost every time.

Which Finance Route Fits Your Peckham Property - by Postcode?

Property type and location shape the right finance decision as much as credit score or income. Here's how different Peckham and South East London addresses typically map to financing options, based on current valuation and equity data.

📊 Buildaway equity calculator - Peckham postcodes: Based on HM Land Registry and Rightmove data (April–May 2026), here's how much a homeowner at 75% LTV could typically access in additional borrowing, assuming a 50% LTV outstanding mortgage:

| Property Type | Area | Avg Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Victorian terrace | SE15 (Choumert, Bellenden) | £420k–£580k | £105k–£145k | Remortgage or Further Advance |

| Edwardian semi-detached | SE22 (East Dulwich, Friern Rd) | £650k–£900k | £162k–£225k | Further Advance or Remortgage |

| Period terrace | SE5 (Camberwell, Coldharbour) | £400k–£600k | £100k–£150k | Second Charge (if mid-fix) |

| Victorian end-of-terrace | SE15 5 (Peckham Rye) | £500k–£720k | £125k–£180k | Any route; remortgage most flexible |

| Smaller flat/terrace | SE15 2 (Peckham town centre) | From £350k | From £87k | Personal loan for smaller projects |

*Assumes 50% LTV outstanding balance; figures indicative only. Always seek independent mortgage advice.

SE22 East Dulwich and the SE15 conservation corridors - special considerations. Properties within the Holly Grove Conservation Area near Peckham Rye station, or the Glengall Road Conservation Area in the heart of SE15, carry design restrictions that lenders take seriously. Some will require full planning permission before releasing funds, because heritage constraints directly affect build viability and therefore the property's value as security. If your home falls within a designated conservation area, start your pre-application conversation with Southwark Council before approaching any lender.

🔑 Citation capsule: Homeowners in SE22 East Dulwich - where four-bedroom Victorian semis regularly reach £700,000–£900,000 - typically hold the largest equity positions and qualify for the most competitive further advance and remortgage rates available to Peckham-area borrowers (HM Land Registry, April 2026). Properties in SE15's designated conservation areas may require planning approval before lenders release funds, adding 8–12 weeks to the project timeline.