Eltham's property market has quietly become one of the standout performers in South East London. House prices across SE9 and SE12 rose 14.1% in the 12 months to April 2026, reaching an average of £507,000 — and a great many homeowners in the area are sitting on equity they haven't properly accounted for (HM Land Registry / Rightmove, Q1 2026).

That equity matters because a single-storey extension here now costs £35,000–£90,000. Very few families have that sitting in a current account. But the relevant question isn't whether you can afford to extend — it's which finance route costs you the least to get there.

Related guide: How much a home extension costs in Eltham

This guide unpacks every option: remortgage, further advance, second-charge mortgage, and personal loan. Crucially, it maps each route to the specific streets and property types you find across Eltham — from the Edwardian terraces behind Well Hall Road in SE9 2 to the semi-detached postwar stock around Avery Hill in SE9 3, and the conservation-adjacent properties near Eltham Palace in SE9 1.

TL;DR:

Single-storey extensions in Eltham cost £35,000–£90,000 in 2026. With house prices up 14.1% year-on-year and the SE9 average sitting at £507,000 (HM Land Registry, Q1 2026), most homeowners hold far more usable equity than they expect. Remortgaging at current 5-year fixed rates of 4.25–4.50% typically beats personal borrowing by thousands. If you're mid-deal on a competitive rate, a further advance or second-charge mortgage often makes more sense.

Why Eltham Homeowners Are Choosing to Extend Rather Than Move

Moving in 2026 is expensive in ways that didn't exist five years ago. Stamp duty on a £600,000 Eltham property comes to £22,500 before you've agreed a sale price. Add estate agent fees (£9,000–£15,000), conveyancing (£2,000–£4,000), and the practical cost of uprooting — and you're looking at £33,000–£45,000 spent before you unpack a single box.

An extension costs a comparable amount — but it builds value rather than consuming it. Extensions across South East London typically return £1.20–£1.50 for every £1 spent and add 10–20% to property value (RICS, 2025). On an average Eltham home at £507,000, that translates to roughly £50,700–£101,400 in added equity.

The numbers are part of it. But there's something else specific to Eltham: many SE9 homeowners bought at prices that felt like a stretch at the time. Now, with values up sharply, they're not quite ready to sell — but their homes don't fit the life they've built. Extending is the logical move.

Around 24% of UK homeowners who seriously considered moving in early 2026 chose to extend instead, citing the disruption and transaction costs as the deciding factor (Quick Move Now, Q1 2026). Walk the planning portal for roads near Court Road or along the Eltham Palace Road corridor and that trend is visible on almost every street.

Cormac Hegarty, Director at Buildaway: "The SE9 and SE12 homeowners we work with have usually already ruled out moving. What they want is more space for the family, and they want it without burning a year of equity on stamp duty and agents. That's exactly the conversation this guide is designed to help you navigate."

Eltham's 14.1% price growth over the past year — against a broader London average decline of 3.3% over the same period (ONS, Feb 2026) — means homeowners here are in a genuinely stronger position than those in many other parts of the capital. The equity base for extension finance is real.

🔑 Citation capsule: Eltham house prices rose 14.1% in the 12 months to April 2026, reaching an average of £507,000 across SE9 and SE12 (HM Land Registry / Rightmove, Q1 2026). Extensions in South East London return £1.20–£1.50 for every £1 spent and typically add 10–20% to property value (RICS, 2025) — making an Eltham extension both a practical and financial upgrade for most homeowners.

How Much Does a Home Extension Actually Cost in Eltham in 2026?

Getting your budget right before approaching a lender is non-negotiable. The South East London construction market runs 20–40% above the national average — a gap that catches homeowners off guard when the first quotes arrive.

In 2026, single-storey extensions in our area cost £2,800–£4,500 per m², versus £2,000–£2,800 nationally (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A 20m² rear extension on a typical SE9 3 semi-detached — a very common project type in Eltham — realistically runs £56,000–£90,000 once you factor in professional fees, building control, and a proper contingency.

Don't underestimate the extras. Many Eltham terraces — particularly the Edwardian stock along Well Hall Road and Glenesk Road in SE9 1 — sit in close proximity to neighbouring properties, making a party wall agreement almost certain. Budget £1,000–£2,500 per neighbouring property for a surveyor. Planning fees start at £206 for a standard householder application. Building control runs £400–£2,000 depending on the scope of work.

Properties near Eltham Palace or within the Eltham Park conservation boundary (SE9 1) face additional requirements from the Royal Borough of Greenwich, which can push architect fees higher and extend the design phase.

The planning approval picture remains encouraging: 87% of householder applications in England were granted in the year to September 2025 (DLUHC, Dec 2025). Most well-prepared Eltham extension applications go through.

Related guide: Single vs Double Storey Extension Guide for Eltham

🔑 Citation capsule: In London and South East England, single-storey home extensions cost £2,800–£4,500 per m² in 2026 — around 20–40% above the national average. A typical 20m² rear extension on an SE9 semi-detached runs £56,000–£90,000 in total project cost including professional fees and contingency (RICS BCIS, 2025; getestimateai.co.uk, March 2026). Underestimating this figure is the single biggest reason projects stall mid-build.

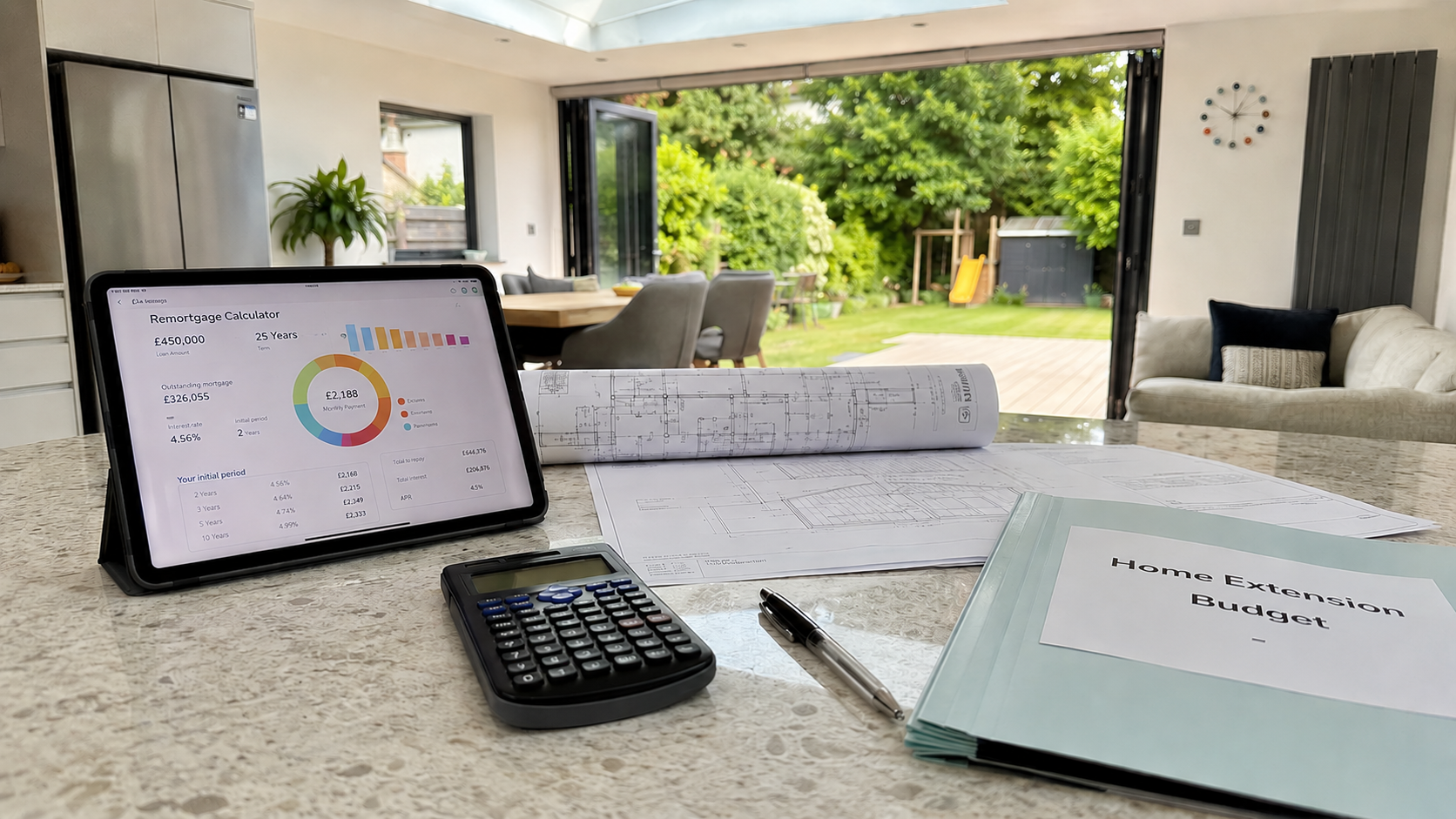

Should You Remortgage to Fund Your Eltham Home Extension?

Remortgaging is the first option most SE9 homeowners consider — and when the timing lines up, it's often the most straightforward way to release extension funding.

The mechanics are simple: your existing mortgage is replaced by a new, larger one. The cash difference between the two is released for your build. In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Even at 75% LTV, those rates remain considerably cheaper than unsecured borrowing.

When does remortgaging work best?

It works best when your current fixed deal is coming to an end. UK Finance estimates that around 1.8 million fixed-rate mortgages are due to expire in 2026 — many of them locked in at sub-2% rates back in 2021. If that describes your situation, your deal is ending regardless. Remortgaging lets you lock in a competitive new rate and release extension capital at the same time, in a single application.

Doing nothing at the end of a fixed deal means rolling onto your lender's Standard Variable Rate, which currently averages 6.49–7.00% (HomeOwners Alliance, May 2026). For a £280,000 outstanding mortgage, the jump from 1.8% SVR adds roughly £1,300 per month. Remortgaging at 4.25% and pulling out £65,000 for an extension can cost almost the same monthly as drifting onto SVR and doing nothing at all.

Watch out for Early Repayment Charges

Mid-deal homeowners need to run the numbers carefully. An ERC of 3% on a £280,000 balance is £8,400. If remortgaging saves £250/month in interest, it takes 34 months just to break even — by which point your deal would likely have ended anyway. In that scenario, a further advance or second-charge mortgage is usually the smarter path.

💡 Our finding: Eltham's 14.1% price growth in the year to April 2026 significantly outpaced the broader London market, which fell 3.3% over the same period (ONS, Feb 2026). For SE9 homeowners, this means LTV positions have improved materially — which in practice unlocks better remortgage rates and larger potential borrowing amounts than they'd expect based on their original purchase price.

The 6-month window: You can lock in a new remortgage rate up to 6 months before your current deal expires — no ERC, no obligation to complete early. If your fix ends before November 2026, now is the time to begin that conversation with a broker.

Remortgaging grew 13.7% in 2025 to 1.86 million refinancing loans (UK Finance). The market is active; using a broker who understands the SE9 and SE12 market is worth the fee.

Related guide: Planning Permission for an Eltham Home Extension

🔑 Citation capsule: In May 2026, competitive 5-year fixed remortgage rates stand at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026; Bank of England, May 2026). UK Finance estimates 1.8 million fixed-rate mortgages will expire in 2026 — many held by homeowners who locked in below 2%. For Eltham homeowners, this creates an ideal window to remortgage and release extension funding simultaneously.

What Is a Further Advance — and When Does It Make Sense for SE9 Homeowners?

A further advance means borrowing additional money from your current mortgage lender — layered on top of your existing deal, without triggering an Early Repayment Charge. It's the option that works precisely when remortgaging doesn't — and it's underused.

The case for it is straightforward. If you've got 18 months left on a 1.9% fix, breaking that deal to remortgage at 4.25% costs you dearly in both ERCs and a higher rate on your entire balance. A further advance lets your existing mortgage sit exactly where it is. Your lender simply adds a second loan on top — secured against the same property, at current market rates — leaving the original deal completely intact.

What the process looks like:

Approval is typically faster than a full remortgage — often 2–4 weeks — because you're already a known customer with an established payment history. The paperwork is leaner. You won't need a new solicitor in most cases. The rate on a further advance sits slightly above your existing mortgage rate but well below unsecured borrowing.

The limitation is availability: not every lender offers further advances, and the maximum borrowable amount may be capped.

If your current lender won't play ball, a second-charge mortgage (Option 3) achieves the same practical outcome without touching your existing deal.

🏡 Buildaway tip: Homeowners in SE9 1 — particularly on streets near Eltham Palace, Court Road, and the Glenesk Road area — tend to hold the strongest LTV positions. Properties on Court Road average £622,000 (HM Land Registry, Q1 2026), giving these homeowners both the equity headroom and the LTV ratio to access the most competitive further advance terms from mainstream lenders.

Always get a written decision in principle before locking in a build timeline. Good Eltham builders are booking weeks ahead. Confirm finance first; sign contracts second.

Related guide: How long a home extension takes in Eltham

Option 3: Secured Loan (Second-Charge Mortgage) — When It's the Right Tool

A second-charge mortgage is a standalone loan secured against your home that sits behind your first mortgage as a separate charge. It doesn't touch your existing deal. It doesn't trigger an ERC. And it's the right choice in several situations that are common across the Eltham area.

In 2026, second-charge rates typically run 4.5–7% depending on LTV and credit profile (Fox Davidson, Jan 2026; ResiQuote, April 2026). That's higher than the best remortgage pricing, but the trade-off is explicit: your current mortgage deal stays completely unchanged. Combined LTV across both loans can't typically exceed 75–85% with mainstream lenders.

This route suits you if:

- You're locked into a low fixed rate with a large ERC still running

- Your income situation is more complex — self-employment, contracting, or irregular earnings

- You need funds faster than a full remortgage allows

- Your current lender doesn't offer further advances at a competitive rate

Eltham's strong professional commuter base — with quick DLR and rail access to Canary Wharf and London Bridge — means self-employed contractors and finance professionals are well represented in the local homeowner mix. Specialist second-charge lenders often assess income more flexibly than the standard remortgage underwriting process.

One honest caution: your property secures both loans. If either becomes unserviceable, both are at risk. This isn't an argument against the route — it's an argument for doing the affordability maths properly before committing.

🔑 Citation capsule: A second-charge mortgage — sometimes called a secured loan — is a separate loan secured against your property equity, sitting behind your existing mortgage. For Eltham homeowners mid-fix on a low rate, it offers a way to borrow £35,000–£90,000 for an extension at 4.5–7% in 2026 without disturbing the existing deal or incurring an ERC (Fox Davidson, January 2026; ResiQuote, April 2026).

When Does a Personal Loan Work for an Eltham Extension?

A personal loan is the simplest route of all — no property valuation, no solicitor, no equity calculation. But it only makes financial sense at the lower end of the cost spectrum.

In 2026, personal loan rates for borrowers with strong credit run 6–10%, with the best pricing available on amounts between £7,500 and £25,000 (ResiQuote, April 2026). Maximum repayment terms typically cap at 7 years — which means monthly payments that are significantly higher than a mortgage-based route spread over 20–25 years.

To put it in concrete terms: £25,000 borrowed at 7% over 5 years costs roughly £495/month with total repayments of around £29,700. That same amount remortgaged at 4.25% over 20 years costs far less each month, though the total interest paid is higher over the extended term. The right answer depends on your cash flow and how long you plan to hold the debt.

When a personal loan makes sense in Eltham:

If you're planning a smaller utility or home office addition — say a £12,000–£18,000 project on a terrace in SE9 4 or SE9 5 — a personal loan is genuinely fast, clean, and doesn't put your property equity at risk. It's also reasonable when you want to keep your renovation finances entirely separate from your mortgage.

What it's not suited for: the typical Eltham extension project. A rear or side-return extension here costs £56,000–£90,000 in total. At that level, a secured route almost always wins on overall cost.

Which Finance Route Fits Your Eltham Property — by Postcode?

No generic finance guide can answer this for you — because the right route depends as much on your street and property type as it does on your credit profile. Here's how SE9 and SE12 break down.

📊 Buildaway equity estimate — Eltham postcodes: Based on HM Land Registry and Rightmove data (Q1 2026), indicative additional borrowing available at 75% LTV assuming 50% LTV outstanding mortgage:

| Property Type | Area | Avg Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Edwardian terrace | SE9 1 (Well Hall, Palace Rd) | £520k–£650k | £130k–£162k | Remortgage or Further Advance |

| 1930s semi-detached | SE9 2 (Eltham Green, Middle Park) | £480k–£580k | £120k–£145k | Further Advance or Remortgage |

| Postwar semi/terrace | SE9 3 (Avery Hill, New Eltham fringe) | £420k–£530k | £105k–£132k | Second Charge (if mid-fix) |

| Detached / larger semi | SE9 4 (Mottingham border, Court Rd) | £520k–£680k | £130k–£170k | Any route; remortgage most flexible |

| Smaller terrace/flat | SE9 5 / SE9 6 | From £380k | From £95k | Personal loan for sub-£25k projects |

| Edwardian/interwar semi | SE12 (Lee, Grove Park) | £450k–£550k | £112k–£137k | Further Advance or Remortgage |

\*Assumes 50% LTV outstanding balance; figures indicative only. Always seek independent mortgage advice.

SE9 1 and the Eltham Palace conservation area — a special case. Properties within the Eltham Park conservation zone, or those on streets directly overlooking Eltham Palace, fall under stricter Royal Borough of Greenwich design guidance. Some lenders require full planning permission before releasing funds in these locations, because build restrictions affect viability and therefore the value of the property as security. If you're in SE9 1 near the Palace, start your planning pre-application discussion with Greenwich Council before approaching a lender.

🔑 Citation capsule: The most suitable finance route for an Eltham home extension depends on postcode and property type. SE9 1 properties near Court Road average £622,000 (HM Land Registry, Q1 2026), giving those homeowners the deepest equity positions and the strongest access to competitive remortgage and further advance rates. Conservation area properties near Eltham Palace may require planning approval before lenders will release funds.