Dartford homeowners sit in a position most of Greater London envies: a 28-minute train to London Bridge, family homes with proper rear gardens, and property values still grounded in reality. The average house price in Dartford stood at £349,000 in January 2026, holding essentially flat against the prior year (ONS / HM Land Registry, Jan 2026).

That stability masks a real opportunity. For homeowners on Temple Hill, along Wentworth Drive, or in the Wilmington villages, that £349,000 figure represents years of mortgage repayment translating into genuine equity — equity that can fund the open-plan kitchen, extra bedroom, or usable rear reception room that a growing family actually needs.

Related guide: How much a home extension costs in Dartford

This guide covers every finance route available to Dartford homeowners in 2026: remortgage, further advance, second-charge mortgage, and personal loan. It also maps each option against the specific property types and planning realities across DA1, DA2, DA3, and DA4 — including the Green Belt constraints that affect rural postcodes differently from anywhere else in this series.

TL;DR:

A single-storey extension in Dartford costs £30,000–£76,000 in 2026, with Kent South East pricing running below inner London but still materially above the national average. With Dartford's average house price at £349,000 (ONS, Jan 2026), most DA1–DA4 homeowners hold enough equity to fund one through secured borrowing. Remortgaging at 5-year fixed rates of 4.25–4.50% typically saves thousands over personal finance. Mid-deal on a low rate? A further advance or second-charge mortgage usually wins on cost.

Why Are Dartford Homeowners Choosing to Extend Rather Than Move?

Moving house in 2026 is expensive — in Dartford, the cost is real even if the stamp duty is lower than in London boroughs.

Consider a typical DA1 homeowner moving from a £350,000 terrace to a £500,000 semi to get more space. Stamp duty alone on the purchase runs to £15,000. Stack on estate agent fees of £7,000–£11,000 on the sale, conveyancing costs of £2,000–£3,500, and the logistical cost of moving, and you're looking at £25,000–£30,000 in transaction costs before you've touched a paintbrush — without guaranteeing a school catchment or commute that works as well as the one you already have.

An extension recycles that spending into the asset you already own. Extensions in the South East typically return £1.20–£1.50 for every £1 spent, adding 10–20% to property value (RICS, 2025). On a £367,000 DA1 home, that represents £43,800–£73,400 in added equity — money that comes back to you at sale, rather than disappearing into an agent's commission.

The commuter calculus matters enormously here. Dartford's fast Southeastern services to London Bridge and Cannon Street are the reason most families are here at all. Moving further into Kent for more space risks losing that sub-30-minute commute window — and the salary premium that comes with it. Around 24% of UK homeowners who seriously considered moving in early 2026 chose to extend instead, citing disruption and transaction costs as the deciding factors (Quick Move Now, Q1 2026). In Dartford, protecting the commute is often the factor that tips the decision.

Cormac Hegarty, Director at Buildaway: "Dartford families come to us once they've run the numbers. The transaction costs are real, but what stops most people isn't the stamp duty — it's the fear of losing a commute that took years to optimise, and disrupting a school run that finally works. The extension conversation usually starts with 'we've decided we're staying.'"

Dartford's property market provides a further argument. Values held essentially flat — up just 0.4% year-on-year to January 2026 (ONS, Jan 2026) — while the Ebbsfleet Garden City development continues to raise the area's long-term desirability. Extending now, before Ebbsfleet-driven amenity improvements fully feed through to surrounding property values, is a well-timed move.

🔑 Citation capsule: Extensions in the South East typically return £1.20–£1.50 for every £1 spent and add 10–20% to property value, according to the Royal Institution of Chartered Surveyors (RICS, 2025). For the average Dartford homeowner at £349,000, this equates to £34,900–£69,800 in added equity — a return that materially outperforms most financing costs, particularly on mid-range DA1 and DA2 projects.

How Much Does a Home Extension Actually Cost in Dartford in 2026?

Knowing your total project cost before approaching a lender is the single most important step in this process. Quote surprises mid-project are how homeowners end up on expensive short-term bridging arrangements.

Dartford sits within Kent rather than Greater London, which places it at the lower end of the South East pricing band. In 2026, single-storey extensions across Kent and the outer South East cost £2,500–£3,800 per m², compared to £2,800–£4,500 for inner South East London boroughs and £2,000–£2,800 nationally (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A 20m² rear extension on a typical DA1 semi-detached runs £50,000–£76,000 once professional fees, building control, and a sensible contingency are included.

Don't overlook the soft costs. Party wall agreements are standard for semi-detached and terraced homes — budget £1,000–£2,000 per adjoining property. Planning fees for a householder application start at £206. Building control runs £400–£1,800 depending on the scope of the project.

Dartford Borough Council processed 572 planning decisions in the year ending September 2025, approving 81.8% of applications (BILTD / Dartford BC, April 2026). That approval rate is solid, though slightly below the national 87% — a reflection of the borough's six conservation areas and significant Green Belt coverage that tighten the rules for some properties. Getting your design right before submission matters more here than in boroughs with fewer constraints.

Underestimating your total project cost by even £10,000 mid-build creates real problems. It's the scenario most likely to push a homeowner toward expensive emergency borrowing.

Related guide: Single vs Double Storey Extension Guide

🔑 Citation capsule: In Dartford and the wider Kent South East market, single-storey home extensions cost £2,500–£3,800 per m² in 2026 — below inner South East London pricing but still 15–30% above the UK national average. A standard 20m² rear extension in DA1 or DA2 therefore runs £50,000–£76,000 in total project cost including professional fees and contingency. Dartford Borough Council approved 81.8% of planning applications in the year ending September 2025 (RICS BCIS, 2025; BILTD, April 2026).

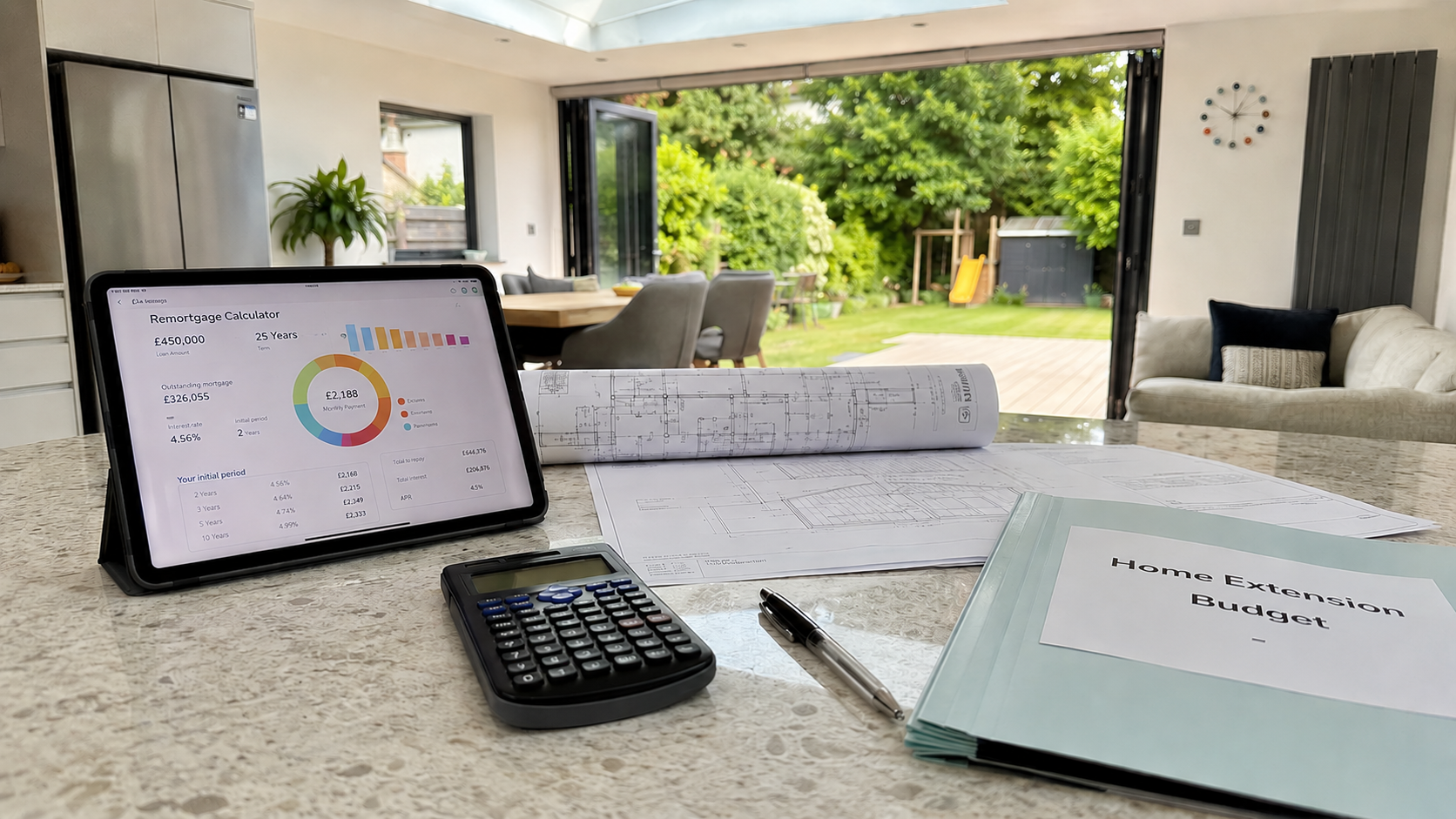

Should You Remortgage to Fund Your Dartford Home Extension?

For most Dartford homeowners whose current deal is coming to an end, remortgaging is the most straightforward and cost-effective way to release extension funding.

The mechanics are simple: replace your existing mortgage with a larger one, and use the difference to fund the build. In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Even at 75% LTV, these rates undercut personal borrowing by a considerable margin.

The strongest window to act

The timing argument is compelling. UK Finance projects that 1.8 million fixed-rate mortgages will expire in 2026 — a significant portion belonging to Dartford homeowners who locked in below 2% in 2020 or 2021. For these borrowers, the deal is ending regardless. A remortgage now lets you set a new rate and release your extension budget in a single transaction.

The alternative — staying put and drifting onto the lender's Standard Variable Rate — is costly. SVRs currently average 6.49–7.00% (HomeOwners Alliance, May 2026). On a £250,000 outstanding mortgage, that's an additional £1,000–£1,200 per month compared to a 1.8% fix. Remortgaging to 4.25% and releasing £55,000 for an extension can cost almost the same monthly as doing nothing and drifting onto SVR.

Weighing Early Repayment Charges mid-deal

If you're still within a fix, the ERC calculation matters. Paying a £5,000 ERC to remortgage at a rate saving £150 per month takes nearly three years to break even. In that scenario, a further advance or second-charge mortgage is usually smarter — both leave your existing rate completely intact.

💡 Our finding: Dartford's property market held essentially flat in the year to January 2026 (+0.4%) while many comparable South East commuter markets showed more movement. For homeowners who bought in DA1 or DA2 a decade ago, that steadiness reflects genuine equity accumulation from mortgage repayment rather than price appreciation alone — making LTV positions here more robust than a flat market headline might suggest.

The 6-month rule: You can lock in a new remortgage rate up to 6 months before your deal expires, with no ERC and no obligation to switch early. If your current fix ends before November 2026, the optimal window to apply is now.

Related guide: Planning Permission for a Dartford Home Extension

🔑 Citation capsule: In May 2026, competitive 5-year fixed remortgage rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026; Bank of England, May 2026). UK Finance projects 1.8 million fixed-rate mortgages will expire in 2026, many belonging to homeowners who locked in below 2% in 2020–21 — creating a primary window for DA1 and DA2 homeowners to remortgage for extension funding without triggering an Early Repayment Charge.

What Is a Further Advance — and Is It Right for Dartford Homeowners?

A further advance is additional borrowing from your existing lender, stacked on top of your current mortgage without disturbing the deal underneath. Of all the finance routes available to Dartford homeowners, it's the one most frequently underestimated — and for mid-deal borrowers on favourable rates, it's regularly the best option on the board.

The mechanism is clean: your existing mortgage carries on exactly as it is. The lender creates a new borrowing facility alongside it, secured against the same property, at a current market rate. You keep your existing rate — including any sub-2% fix that still has years to run — while accessing extension funding separately.

What the process looks like in practice

The application is simpler than a full remortgage because you're already a known customer. Processing typically takes 2–4 weeks, and some lenders can move faster when the amount is modest and the LTV is comfortable. The rate will sit above your existing mortgage rate but well below personal borrowing.

One limitation: not every lender offers further advances, and those that do may cap the amount based on internal LTV thresholds. If your current lender won't play ball at a competitive rate, a second-charge mortgage achieves the same outcome — your main deal stays untouched while a separate secured facility provides the extension budget.

🏡 Buildaway tip: Homeowners in DA3 (Longfield, Hartley) and DA4 (Farningham, Eynsford) tend to hold significantly lower LTV ratios than town-centre postcodes. Larger detached homes in these areas often carry outstanding balances well below 50% of current value, particularly for owners who purchased in the 2010s. That sub-40% LTV profile unlocks the most competitive further advance tiers from mainstream lenders — rates very close to what a clean remortgage would deliver.

Always get a written decision in principle before committing to any build timeline. Dartford extension contractors are booking weeks ahead. Confirmed finance should come before you sign contracts.

Related guide: How long a home extension takes in Dartford

Option 3: Secured Loan (Second-Charge Mortgage) — When It Fits a Dartford Situation

A second-charge mortgage is a separate secured loan that sits behind your primary mortgage in priority order — it uses the same property as collateral but runs entirely independently from your existing deal. It's the right tool when the cost of breaking your current mortgage outweighs the benefit of remortgaging.

In 2026, second-charge rates typically run 4.5–7.0% depending on LTV and credit profile (Fox Davidson, Jan 2026; ResiQuote, April 2026). Those rates are higher than the best remortgage deals, but the trade-off is straightforward: your existing mortgage stays exactly as it was, regardless of what rate or term it carries. Combined LTV across both loans typically cannot exceed 75–85% with mainstream lenders.

When this route makes sense for a Dartford homeowner:

- You're locked into a 2021 fix at a rate well below 4% with a significant ERC still outstanding

- You're self-employed or have recently changed income structure — common for Dartford's commuter population who often move between employment and consulting arrangements

- You want funds in place faster than a full remortgage typically allows

- Your current lender doesn't offer further advances or won't approve the amount you need

Dartford draws a significant proportion of self-employed professionals — City workers who've moved to contracting, tradespeople running their own businesses, and Kent-based business owners who commute into London. Second-charge lenders assess income more flexibly than high-street remortgage underwriting, which has genuine practical value for anyone whose income isn't straightforward salaried employment.

One clear point: both loans are secured against your home. If either becomes unserviceable, both are at risk. That's not a reason to avoid the route — but it is a reason to stress-test your monthly budget before committing.

🔑 Citation capsule: A second-charge mortgage sits behind your primary loan and allows Dartford homeowners to borrow against built-up property equity at rates of 4.5–7% in 2026, without touching the existing mortgage deal. Combined LTV across both loans typically cannot exceed 75–85% with mainstream lenders — a threshold most DA1 and DA2 homeowners are positioned to meet (Fox Davidson, January 2026; ResiQuote, April 2026).

When Does a Personal Loan Make Sense for a Dartford Extension?

A personal loan carries one real advantage over every secured route: there's no property valuation, no solicitor, and no underwriting that references your home. For smaller, well-defined projects, that speed and simplicity is worth something.

In 2026, personal loan rates run 6–10% for borrowers with good credit, with the best deals available on amounts between £7,500–£25,000 (ResiQuote, April 2026). Repayment terms are capped at 7 years, pushing monthly payments higher than any mortgage-based equivalent over 20+ years.

The comparison: £20,000 borrowed over 5 years at 7% costs roughly £396/month, with total repayments around £23,800 — £3,800 in interest. The same amount remortgaged at 4.25% over 20 years costs considerably less each month, though the total interest paid rises with the extended term.

When a personal loan is genuinely the right call:

For a utility room addition at the back of a DA1 terrace running around £12,000–£18,000, a personal loan is quick, clean, and avoids the administrative weight of a remortgage or secured loan. It's also worth considering when you want your renovation budget to stay entirely separate from your property equity — some homeowners simply prefer that separation.

What it doesn't suit: the typical Dartford rear extension. Single-storey projects here run £50,000–£76,000. At that scale, secured finance wins on total cost in almost every scenario. The crossover point where personal loans become competitive sits at roughly £20,000 and below.

Which Finance Route Fits Your Dartford Property — by Postcode?

Dartford's DA postcodes cover a wide range of property types and values — from town-centre terraces in DA1 to semi-rural detached homes in the Green Belt fringe of DA4. The right finance route shifts considerably across this range.

📊 Buildaway equity guide — Dartford postcodes: Based on HM Land Registry and ONS data (April–May 2026), here is how much a homeowner at 75% LTV could typically access in additional finance, assuming a 50% LTV outstanding mortgage:

| Property Type | Area | Avg Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Post-war semi-detached | DA1 (Temple Hill, West Hill) | £380k–£470k | £95k–£117k | Remortgage or Further Advance |

| Victorian/Edwardian terrace | DA1 (Priory Hill, Hythe St area) | £320k–£400k | £80k–£100k | Further Advance or Remortgage |

| Period/semi in conservation village | DA2 (Wilmington, Sutton-at-Hone) | £400k–£550k | £100k–£137k | Second Charge (if mid-fix) |

| Detached / rural character | DA3 (Longfield, Hartley) | £450k–£650k | £112k–£162k | Any route; remortgage most flexible |

| Green Belt / larger detached | DA4 (Farningham, Eynsford) | £500k–£800k+ | £125k–£200k | Specialist broker recommended |

*Assumes 50% LTV outstanding balance; figures indicative only. Always seek independent mortgage advice.

DA4 Farningham and Eynsford — the Green Belt caveat. Properties in DA4 sit in some of the most scenic countryside in North West Kent, with detached homes regularly exceeding £600,000. The equity headroom is substantial. However, two complications apply. First, Green Belt designation restricts what extensions are permissible — Dartford Borough Council will not approve works that materially harm the rural character of the area, and proposals must demonstrate exceptional design sensitivity. Second, lenders value Green Belt properties differently. If planning restrictions limit the scope of the permitted extension, some lenders adjust their advance to reflect a more conservative view of the property as security. Always instruct an architect familiar with DBC's Green Belt policies before approaching any lender.

Properties in Dartford's conservation areas — Wilmington village, Sutton-at-Hone, and the Dartford town centre historic core — face similar considerations: some lenders require planning approval from Dartford Borough Council before funds are released, particularly where heritage sensitivity affects build viability.

🔑 Citation capsule: Dartford Borough Council administers six conservation areas including Wilmington village and Sutton-at-Hone, and significant Green Belt coverage across DA3 and DA4 postcodes. Planning applications in these areas face a tighter approval environment — DBC approved 81.8% of applications in the year ending September 2025, below the national average of 87%. For DA4 Green Belt properties, specialist mortgage advice is strongly recommended before approaching lenders (Dartford Borough Council / BILTD, April 2026; DLUHC, December 2025).