In early 2026, the average house price in Clapham reached £723,000 — and for homeowners across SW4, SW11, and SW12, that figure represents years of equity growth sitting tied up in period properties while families run out of room (HM Land Registry, Feb 2026).

A single-storey extension in inner South West London now costs £38,000–£95,000. That is not a sum most households have sitting in a current account. So the real question is rarely "can I afford to extend?" — it's "which finance route costs me the least, and when should I start?"

Related guide: How much a home extension costs in Clapham

This guide covers every realistic option: remortgage, further advance, second-charge mortgage, and personal loan. Crucially, it maps each route to the specific property types found across Clapham — from the Victorian terraces lining Narbonne Avenue and Abbeville Village in SW4, to the Edwardian semis on the streets behind Northcote Road in SW11.

TL;DR:

A single-storey extension in Clapham costs £38,000–£95,000 in 2026. With average house prices at £723,000 (HM Land Registry, Feb 2026), the majority of SW4–SW12 homeowners hold more than enough equity to fund one. Remortgaging at today's 5-year fixed rates of 4.25–4.50% is typically the cheapest route overall. If you're locked into a low rate mid-deal, a further advance or second-charge mortgage often preserves far more value.

Why Are Clapham Homeowners Choosing to Extend Rather Than Move?

The financial case against moving has rarely been stronger — and Clapham homeowners are running the numbers. Stamp duty on an £800,000 property now costs £27,500. Add estate agent fees of £12,000–£18,000, conveyancing at £2,500–£5,000, and removals on top, and you're looking at £45,000–£55,000 gone before a single coat of paint goes up in the new place.

That same outlay, redirected into an extension, doesn't disappear — it adds to your home's value. Extensions across inner South West London typically return £1.20–£1.50 for every £1 spent and add 10–20% to property value (RICS, 2025). On a £723,000 Clapham home, that's £72,300–£144,600 in additional equity.

The pattern is visible on the ground. Across Clapham's Victorian terraces — particularly those on the streets feeding off the Common and along Abbeville Road — planning applications for rear and wraparound extensions have become a near-permanent feature of Lambeth and Wandsworth's weekly lists. Around 24% of UK homeowners who seriously explored moving in early 2026 chose to extend instead, with upfront moving costs and disruption cited as the decisive factors (Quick Move Now, Q1 2026).

Cormac Hegarty, Director at Buildaway: "The Clapham homeowners we work with — particularly in SW4 and SW11 — have almost always done the maths before they call us. They know moving means burning £50,000 before they get the keys. The conversation moves almost immediately from 'should we extend?' to 'how do we finance it?' — and that's where we need to give them clear answers."

Clapham's property market has its own microclimate worth understanding: terraced house values in the area have held significantly firmer than the wider London flat market, with Northern Line proximity acting as a consistent floor under per-square-foot values across SW4, according to local market analysis (ValuQ, April 2026). Homeowners with houses — rather than flats — are in the strongest position to access equity finance for an extension.

🔑 Citation capsule: A well-executed home extension in inner South West London typically returns £1.20–£1.50 for every £1 spent and adds 10–20% to property value, according to the Royal Institution of Chartered Surveyors (RICS, 2025). For the average Clapham homeowner at £723,000, this translates to £72,300–£144,600 in added equity — comfortably ahead of financing costs on most project types.

How Much Does a Home Extension Actually Cost in Clapham in 2026?

Before approaching a lender is non-negotiable. Clapham's dense terrace streets mean extensions here carry specific cost drivers that don't show up in national pricing guides.

In 2026, single-storey extensions across London and the South East cost £2,800–£4,500 per m², running 20–40% above the UK national average of £2,000–£2,800 (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A 20m² rear extension on a typical SW4 terrace realistically comes to £56,000–£90,000 once professional fees, building control, and contingency are included. The signature Clapham wraparound — combining rear and side return into one open-plan ground floor — typically runs £65,000–£120,000 depending on specification.

The hidden costs matter here too. Clapham's terrace streets mean virtually every rear or side return extension triggers party wall obligations — budget £1,000–£2,500 per neighbouring property for a surveyor, and Clapham terraces often have neighbours on both sides. Planning fees start at £206 for a standard householder application. Building control runs £400–£2,000 depending on the scope of works. Properties within the Clapham Old Town Conservation Area (Lambeth) or the Northcote Road Conservation Area (Wandsworth) can face more prescriptive design requirements that push architect fees higher.

The broader picture is positive: 87% of householder planning applications in England were granted in the year to September 2025 (DLUHC, Dec 2025). Extensions get approved — but getting your total cost right before approaching a lender avoids the expensive mid-project surprises.

Related guide: Single vs Double Storey Extension Guide

🔑 Citation capsule: In London and the South East, single-storey home extensions cost £2,800–£4,500 per m² in 2026 — 20–40% above the UK national average. A typical 20m² rear extension in Clapham runs £56,000–£90,000 in total project cost, including professional fees and contingency, while a wraparound extension can reach £65,000–£120,000 (RICS BCIS, 2025; getestimateai.co.uk, March 2026).

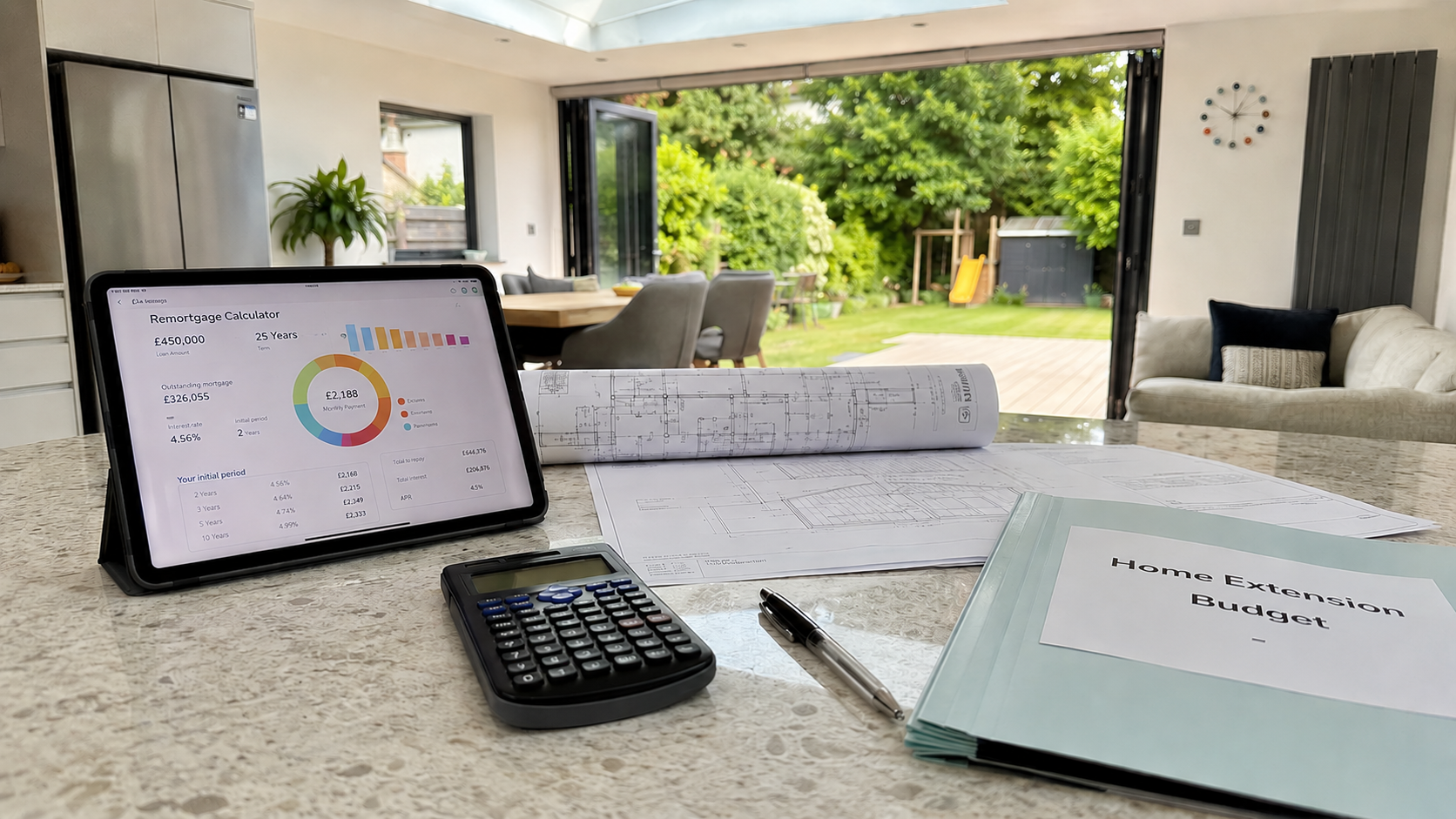

Should You Remortgage to Fund Your Clapham Home Extension?

For most Clapham homeowners whose fixed-rate deal is approaching its end date, remortgaging is the most straightforward and cost-effective route to extension finance.

The mechanics are simple: your existing mortgage is replaced with a larger one, and the difference between the old balance and the new one is released as cash to pay for the build. In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Even at 75% LTV — a common position for Clapham owners who took out larger mortgages on high-value properties — rates remain considerably cheaper than any unsecured borrowing.

When remortgaging makes most sense

It's most powerful when your current deal is ending or has already rolled onto your lender's Standard Variable Rate. UK Finance estimates around 1.8 million fixed-rate mortgages will expire in 2026, many locked in at below 2% in 2021. If yours is one of them, your rate is changing regardless — remortgaging now lets you set a new rate and release extension funds in a single transaction.

The SVR alternative is stark. Lender standard variable rates currently average 6.49–7.00% (HomeOwners Alliance, May 2026). On a £400,000 outstanding Clapham mortgage — not unusual at SW4 property values — drifting onto SVR adds roughly £1,800–£2,000 per month versus a current 1.8% fix. Remortgaging at 4.25% and releasing £70,000 for an extension can cost barely more per month than doing nothing and ending up on SVR.

The Early Repayment Charge consideration

If you're inside a fixed-rate period, the ERC needs careful analysis. Many Clapham homeowners on 2021 deals face ERCs of 1–5% of their outstanding balance — on a £400,000 mortgage, that's potentially £4,000–£20,000. If that figure outweighs the rate saving, a further advance or second-charge mortgage (outlined below) will likely be the smarter move.

💡 Our finding: Within Clapham's property market, the strongest equity positions belong to owners of Victorian houses rather than period-conversion flats. Terraced house values have held notably firmer than the flat market across SW4 — which matters when lenders are calculating LTV for remortgage approval. House owners in streets like Narbonne Avenue, Rodenhurst Road, and Abbeville Village are typically in the most competitive LTV band for remortgage rates.

The 6-month window: You can lock in a remortgage rate up to 6 months before your current deal expires — at no cost and with no obligation to switch early. If your fix ends before November 2026, the right time to apply is now.

Remortgaging volumes grew 13.7% in 2025 to 1.86 million refinancing transactions (UK Finance). The market is active and brokers with South London expertise are worth the fee.

Related guide: Planning Permission for a Clapham Home Extension

🔑 Citation capsule: In May 2026, the Bank of England base rate stands at 3.75%, with competitive 5-year fixed remortgage deals available at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026; Bank of England, May 2026). UK Finance estimates 1.8 million fixed-rate mortgages will expire in 2026 — many belonging to homeowners who fixed below 2% — making this the primary window to remortgage and release extension funding.

What Is a Further Advance — and Is It Right for a Clapham Homeowner?

A further advance means borrowing additional money from your existing mortgage lender — without disturbing your current deal. No ERC. No new valuation on the full property. Your existing rate stays exactly as it is.

For Clapham homeowners who locked in at 1.5–2% in 2021 that runs until 2026, the further advance is the route that preserves the rate worth keeping while still releasing the funds needed to extend. The lender assesses your equity and current affordability, then offers a top-up loan — secured against the same property — at a current market rate, while your low-rate deal runs undisturbed to its natural end.

What to expect in practice

The rate on a further advance will be higher than your existing mortgage rate, but materially lower than a personal loan. Approval is typically faster than a full remortgage — 2–4 weeks in most cases. The underwriting process is also lighter, since you're already an established customer with a tracked payment record.

The limitations: not every lender offers this product, and the maximum borrowing may be capped. If your lender doesn't offer a further advance, or quotes a rate that erases the benefit of protecting your existing deal, a second-charge mortgage achieves the same outcome without touching your main mortgage at all.

🏡 Buildaway tip: Homeowners along Clapham Common North Side, Rodenhurst Road, and the streets immediately off Abbeville Village typically hold lower LTV ratios than the SW4 average — a consequence of holding some of Clapham's most valuable houses with long ownership histories. That reduced LTV often unlocks the most competitive further advance rates and avoids the need for a full remortgage entirely.

Always secure a written decision in principle before committing your build timeline to a contractor. Clapham's most capable builders are working several weeks ahead — confirmed finance should come before contracts are signed.

Related guide: How long a home extension takes in Clapham

Option 3: Secured Loan (Second-Charge Mortgage) — When It Fits

A second-charge mortgage is a separate loan secured against your home that sits behind your primary mortgage in the priority queue. It uses the same property as collateral but has no effect on your existing mortgage terms. For certain Clapham homeowners, this is precisely the right instrument.

In 2026, second-charge rates typically run 4.5–7% depending on credit profile and combined LTV (Fox Davidson, Jan 2026; ResiQuote, April 2026). That's above the best remortgage deals, but the trade-off is structural: your existing mortgage — whatever the rate — stays entirely intact. Most mainstream lenders cap combined LTV across both loans at 75–85%.

This route suits a Clapham homeowner who:

- Holds a sub-2% fix with a meaningful ERC still to run

- Is self-employed or operates as a contractor, where specialist lenders assess income more flexibly than high-street underwriting

- Needs funds more quickly than a full remortgage allows

- Has had an income change since the original mortgage was arranged

Clapham's professional community — finance, media, tech, and a large cohort of contractors — means self-employment is common across SW4 and SW11. Second-charge lenders tend to take a more pragmatic approach to variable and contract income, and that flexibility has genuine value for a significant proportion of the area's homeowners.

One honest note: both your mortgage and the second charge are secured against your home. If either becomes unserviceable, both are at risk. This isn't a reason to avoid the route — it's a reason to ensure the numbers work before you commit.

🔑 Citation capsule: A second-charge mortgage sits behind your existing mortgage and allows Clapham homeowners to borrow against property equity at rates of 4.5–7% in 2026, without affecting their current mortgage deal. The combined LTV across both loans typically cannot exceed 75–85% with mainstream lenders (Fox Davidson, January 2026; ResiQuote, April 2026).

When Does a Personal Loan Make Sense for a Clapham Extension?

A personal loan needs no property valuation, no equity calculation, and no solicitor. For a smaller project, it's fast and clean. But the cost structure only makes it genuinely competitive at the lower end of the budget range.

In 2026, personal loan rates run 6–10% for borrowers with good credit histories, with the sharpest rates available on borrowing between £7,500–£25,000 (ResiQuote, April 2026). Terms cap at 7 years, which means higher monthly repayments than any mortgage-secured equivalent stretched over 20 years.

To illustrate: £25,000 over 5 years at 7% costs roughly £495 per month, with total interest paid of around £4,700. Against the same amount via remortgage at 4.25% over 20 years, the monthly payment drops considerably — though the long term means overall interest paid rises. The optimal route depends on whether monthly cashflow or total interest cost is the bigger constraint.

When a personal loan is the right call for a Clapham homeowner:

A modest utility extension or a compact side return on a SW12 flat — budget £15,000–£22,000 — may well suit a personal loan: quick approval, no property valuation, no legal fees. It also suits homeowners who want to keep their mortgage position entirely separate from their renovation decision.

Where it falls short: the majority of Clapham extensions. A full rear or wraparound extension on a SW4 Victorian terrace will routinely exceed £65,000. At that level, secured borrowing almost always delivers a lower blended cost.

Which Finance Route Fits Your Clapham Property — by Postcode?

The right finance route depends as much on your specific street and postcode as it does on your income or credit score. Clapham spans two London boroughs — Lambeth and Wandsworth — each with its own planning department, conservation area designations, and LTV norms.

📊 Buildaway equity calculator — Clapham postcodes: Based on HM Land Registry data (April–May 2026), here's how much a homeowner at 75% LTV could typically borrow in additional financing, assuming a 50% LTV outstanding mortgage:

| Property Type | Area | Avg Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Victorian terrace | SW4 (Abbeville Village, Narbonne Ave) | £650k–£900k | £162k–£225k | Remortgage or Further Advance |

| Edwardian terrace | SW4 (Clapham Park, Old Town) | £600k–£800k | £150k–£200k | Further Advance or Remortgage |

| Victorian semi-detached | SW11 (Northcote Rd, Lavender Hill) | £800k–£1.2m | £200k–£300k | Second Charge (if mid-fix) |

| Large Victorian / Common-side | SW4 (Common North Side) | £900k–£1.5m+ | £225k–£375k | Any route; remortgage most flexible |

| Flat or conversion | SW4/SW9 (Stockwell border) | From £450k | From £112k | Personal loan for smaller projects |

*Assumes 50% LTV outstanding balance; figures indicative only. Always seek independent mortgage advice.

The conservation area dimension in Clapham. Unlike many London areas with a single planning authority, Clapham homeowners deal with either Lambeth (SW4) or Wandsworth (SW11) — and each has its own conservation area rules and planning character. The Clapham Old Town Conservation Area (Lambeth) covers parts of the Old Town and streets off the Common; the Northcote Road Conservation Area (Wandsworth) covers parts of SW11. Both can require full planning approval before a lender will release funds, since design restrictions affect both build viability and the property's value as security. If you're in either area, initiate the planning conversation with the relevant council before approaching any finance provider.

🔑 Citation capsule: Clapham spans both the London Borough of Lambeth (SW4) and the London Borough of Wandsworth (SW11), with separate planning departments and conservation areas. Victorian house owners in Abbeville Village and along Clapham Common North Side typically hold the most equity relative to outstanding mortgage balances, while conservation area properties in Clapham Old Town and the Northcote Road area may require planning approval before lenders release extension funds (HM Land Registry, April 2026; LCCL Construction, May 2026).