In early 2026, the average house price in Chislehurst reached £729,000 — making BR7 one of the highest-value postcodes in the entire London Borough of Bromley (HM Land Registry / Rightmove, April 2026). For homeowners along roads like Beaverwood Road, Lubbock Road, and Manor Park Road, that number represents substantial locked-in equity. But it also comes with a complication that buyers elsewhere don't face to the same degree: Chislehurst holds the largest conservation area in Bromley, and that changes the extension finance conversation considerably.

A rear extension in South East London costs £35,000–£90,000 depending on size and specification. Few families have that sitting in a current account. So the real question isn't whether you can afford to extend — it's which finance route costs you least, and what you need to sort out before the money can move.

Related guide: How much a home extension costs in Chislehurst

This guide walks through every borrowing route — remortgage, further advance, second-charge mortgage, and personal loan — and maps each one to the types of properties you'll actually find in BR7: Victorian and Edwardian detached houses around Camden Place, 1930s semis on Holbrook Lane, and the larger detached homes backing onto Scadbury Park.

TL;DR:

Home extensions in Chislehurst cost £35,000–£90,000 in 2026. With average BR7 property values at £729,000 (HM Land Registry, 2026), most homeowners hold enough equity to fund one comfortably. Five-year fixed remortgage rates at 4.25–4.50% remain far cheaper than personal borrowing. If you're mid-deal, a further advance or second-charge mortgage often wins — but conservation area properties may need planning approval before any lender will release funds.

Why Are Chislehurst Homeowners Choosing to Extend Rather Than Move?

The economics of upsizing have rarely been more punishing. Stamp duty on a £900,000 Chislehurst property now runs to approximately £37,500 under current SDLT bands. Add estate agent fees of £9,000–£18,000, conveyancing costs, and removal logistics, and you're burning through £50,000–£60,000 before you've even painted a wall — and that's before you account for the fact that the next property up from your current home carries a premium that may simply be out of reach.

Extending doesn't eliminate cost. But it converts spending into equity. Extensions across South East London typically return £1.20–£1.50 for every £1 spent and add 10–20% to property value (RICS, 2025). On a £729,000 Chislehurst home, that's roughly £72,900–£145,800 in added value — comfortably ahead of most financing costs for a well-executed project.

Around 24% of UK homeowners who seriously considered moving in early 2026 chose to extend instead, citing moving costs and disruption as primary drivers (Quick Move Now, Q1 2026). In Chislehurst, the calculus tilts even further toward extending. The village's character, school catchments, and proximity to the Common and Chislehurst Caves make BR7 a postcode people are reluctant to leave — particularly families with children settled into Bullers Wood or Coopers School.

Cormac Hegarty, Director at Buildaway: "Chislehurst is a postcode where people stay. We see it constantly — families who bought a Victorian semi off Old Hill ten years ago have outgrown it, but have no intention of leaving the area. The conversation shifts fast from 'should we move?' to 'what can we add?' — and then straight to 'how do we pay for it?' That's exactly where this guide picks up."

There's a financial dimension specific to BR7 too: Chislehurst property values increased by approximately 1.76% in the 12 months to early 2026 (propertysolvers.co.uk), holding up solidly while wider London averages fell. Homeowners here are sitting on equity that is, pound for pound, stronger than in many comparable London postcodes.

🔑 Citation capsule: A well-executed home extension in South East London typically returns £1.20–£1.50 for every £1 spent, adding 10–20% to property value according to the Royal Institution of Chartered Surveyors (RICS, 2025). For a Chislehurst homeowner at the average BR7 value of £729,000, that translates to £72,900–£145,800 in potential added equity — comfortably ahead of extension financing costs for most single or side-return projects.

How Much Does a Home Extension Actually Cost in Chislehurst in 2026?

Getting your budget right before you approach a lender is essential — running short mid-build is expensive in ways that go beyond just stress. Chislehurst's mix of period architecture and conservation area oversight means costs here often track toward the upper end of the London range.

In 2026, single-storey extensions in London and the South East cost £2,800–£4,500 per m², compared to a national average of £2,000–£2,800 (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A 20m² rear extension on a BR7 semi-detached house therefore runs £56,000–£90,000 in total project cost once you include architect fees, building control, and a sensible contingency.

In Chislehurst specifically, certain costs run higher than you'd see elsewhere in Bromley. The conservation area designation — the largest in the London Borough of Bromley (Chislehurst Society) — means any external alteration requires specific consent, and design briefs must respect the character of the surrounding streetscape. Architects working to conservation area standards typically charge more, and planning applications often need additional heritage justification documents. Budget separately for this.

Party wall matters are also common in the Victorian terraces and Edwardian semis that line Lower Camden and Watts Lane — typically £1,000–£2,500 per shared boundary. Building control runs £400–£2,000 depending on scope and complexity. The householder planning fee starts at £206.

None of this makes extending unviable. Nationally, 87% of householder planning applications in England were granted in the year to September 2025 (DLUHC, Dec 2025). Extensions are approved regularly. But the Chislehurst conservation area does mean a longer runway from concept to site start — which matters for your finance timeline.

Related guide: Single vs Double Storey Extension in Chislehurst

🔑 Citation capsule: In London and the South East, single-storey home extensions cost £2,800–£4,500 per m² in 2026 — 20–40% above the national average. In the Chislehurst conservation area, additional architect fees and heritage compliance can add further cost. A typical 20m² rear extension in BR7 should be budgeted at £56,000–£90,000 in total project cost, including professional fees and contingency (RICS BCIS, 2025; getestimateai.co.uk, March 2026).

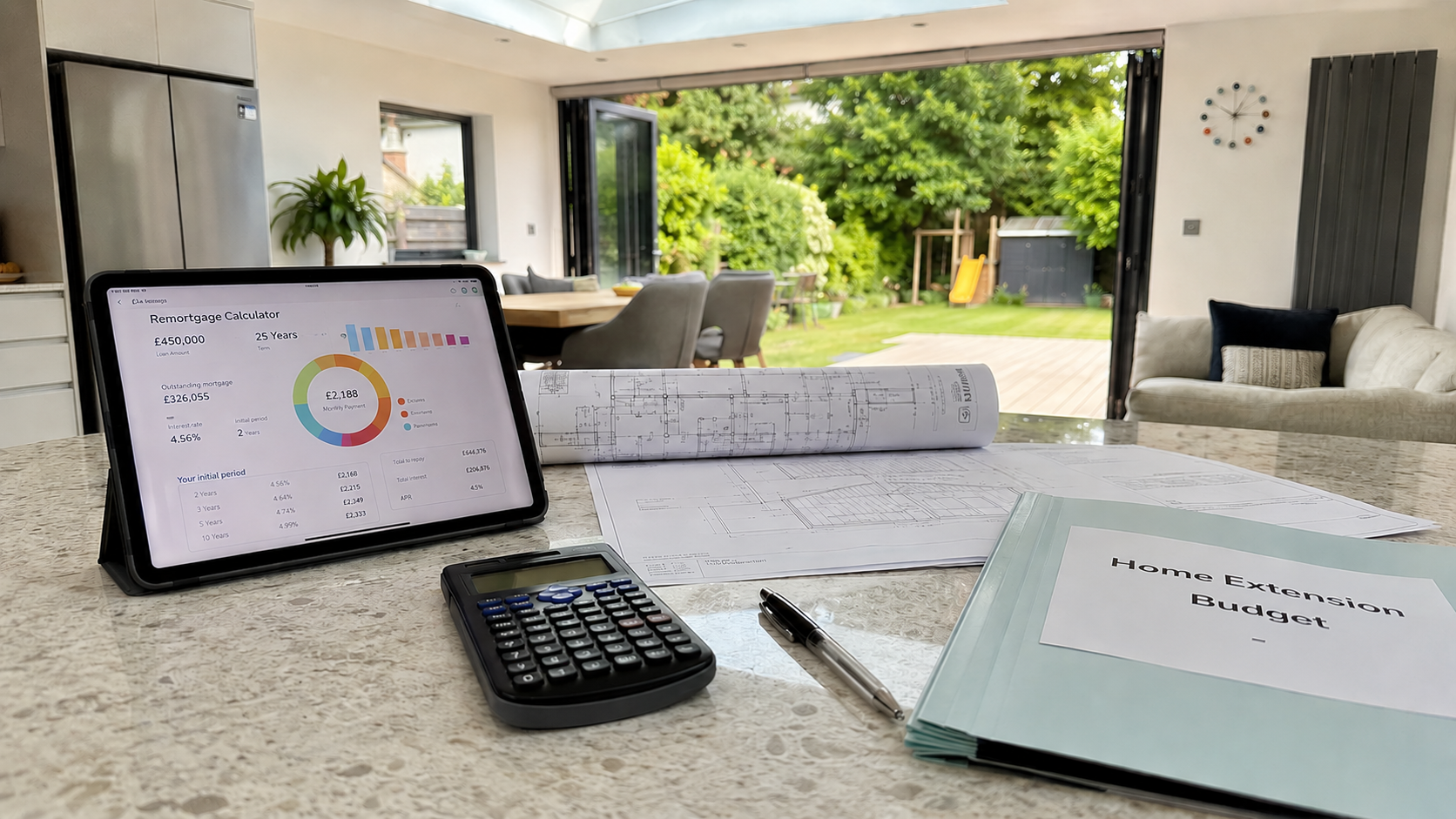

Should You Remortgage to Finance Your Chislehurst Extension?

For homeowners whose fixed rate is ending — or has already ended — remortgaging is almost always the most cost-effective way to raise extension funding. You replace your current mortgage with a larger one, and the difference between the two amounts comes to you as cash to fund the build.

In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Given the equity positions most Chislehurst homeowners hold, many will qualify at 60% LTV or below — unlocking the sharpest rates on the market. That's a meaningful advantage over higher-LTV borrowers elsewhere.

Timing is everything here. According to UK Finance, around 1.8 million fixed-rate mortgages expire in 2026, many held by owners who locked in at below 2% in 2021. If you're one of those homeowners, your deal is ending regardless. Remortgaging now to release extension capital costs you nothing extra in comparison to simply renewing — and gets your project moving.

The alternative — letting your deal lapse onto a Standard Variable Rate — is expensive by any measure. SVRs currently average 6.49–7.00% (HomeOwners Alliance, May 2026). For a £350,000 outstanding balance, that's roughly £1,800 a month more than a well-timed remortgage. Releasing £75,000 for an extension at the same time adds comparatively little to your monthly payment.

Watch out for the Early Repayment Charge. If you fixed at 1.5–2% in 2021 and still have time left to run, your ERC could be 1–5% of your outstanding balance. Paying £8,000 in charges to remortgage into a rate that saves you £250 per month takes well over two years to break even. In that scenario, a further advance or second-charge mortgage is usually cheaper — see Options 2 and 3 below.

💡 Our finding: Chislehurst's average BR7 property value of £729,000 (HM Land Registry, 2026) gives most homeowners an exceptionally strong LTV position compared to the wider London average. A household with a £250,000 outstanding mortgage on a £729,000 home sits at roughly 34% LTV — accessing the very lowest rate tiers. That equity headroom is one of the genuine financial advantages of staying in BR7.

The six-month window: You can lock in a new remortgage rate up to six months before your existing deal expires — paying no ERC and taking on no obligation to switch early. If your fix ends before November 2026, the window to act is now.

Remortgaging activity rose 13.7% in 2025 to 1.86 million refinancing transactions (UK Finance). The market is active; a specialist broker who understands conservation area properties is worth every penny.

Related guide: Planning Permission for a Chislehurst Home Extension

🔑 Citation capsule: In May 2026, the Bank of England base rate stands at 3.75%, with competitive 5-year fixed remortgage rates available at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). With average BR7 house values at £729,000, many Chislehurst homeowners qualify for these sharpest rate tiers — making remortgage one of the most affordable routes to raise home extension capital in the area.

What Is a Further Advance, and When Does It Make Sense in BR7?

A further advance lets you borrow additional money from your existing mortgage lender without touching — or losing — your current deal. It's the option most easily overlooked, and for many Chislehurst homeowners it's actually the smartest move available.

Here's the core logic: if you secured a 1.8% fix that runs until 2027, switching to a remortgage means walking away from that rate. A further advance keeps it. Your lender adds a new loan alongside your existing mortgage — secured against the same property — at a current market rate. The two loans run independently. Your cheap fix stays untouched.

What to expect in practice:

The rate on a further advance typically sits a little higher than your existing mortgage rate, but well below a personal loan. Approval tends to come faster than a full remortgage — many lenders process further advances within 2–4 weeks. Because you're already a known customer with a payment record, underwriting is lighter too.

The practical limitation: not every lender offers them, and the amount you can borrow may be capped based on current income and LTV. If your lender either doesn't offer a further advance or isn't pricing it competitively, a second-charge mortgage (Option 3) gets you to the same outcome without disturbing your existing deal.

🏡 Buildaway tip: Homeowners in the detached and semi-detached streets around Beaverwood Road and Old Hill — where average values have exceeded £885,000 and £1,000,000 respectively (HM Land Registry, April 2026) — often hold LTV ratios well below 50%. That puts them in a strong position to negotiate further advance rates directly with their existing lender, without needing a broker to shop the market.

Always get a written decision in principle before locking in your build timeline. Good Chislehurst extension contractors are typically booked weeks ahead — don't sign a contract without confirmed funding in place.

Related guide: How long a home extension takes in Chislehurst

Option 3: Secured Loan (Second-Charge Mortgage) — When It Suits Chislehurst Homeowners

A second-charge mortgage is a separate loan secured against your property, running alongside your existing mortgage rather than replacing it. It's the right tool when remortgaging would cost more than it saves — and in Chislehurst, where a significant number of homeowners are self-employed or work in professional services, it opens up flexibility that mainstream remortgage underwriting sometimes doesn't.

Rates for second-charge mortgages in 2026 typically fall in the 4.5–7% range, depending on your LTV and credit profile (Fox Davidson, Jan 2026; ResiQuote, April 2026). That's higher than the best remortgage deals — but the calculation shifts when your current mortgage rate is worth protecting. The combined LTV across both loans typically can't exceed 75–85% with mainstream lenders, though specialist lenders can sometimes go further.

This route makes particular sense when:

- You're locked in on a deal worth keeping, with a meaningful ERC still to run

- Your income is variable — contracting, freelance, or self-employed — and specialist lenders assess affordability more sympathetically than high-street underwriters

- You need funding faster than a full remortgage allows

- Your property falls into a specialist category that standard lenders are cautious about

That last point is relevant in Chislehurst. Some lenders treat conservation area properties with additional scrutiny — particularly if the extension design hasn't received planning approval yet. Specialist second-charge lenders are sometimes better positioned to understand the BR7 market and price the risk accordingly.

One thing to be clear-eyed about: your home is security on both loans. If you can't service one, you're at risk on both. That's not a reason to avoid the route — it's a reason to stress-test the numbers before committing.

🔑 Citation capsule: A second-charge mortgage sits behind your existing mortgage in the priority queue but uses the same property as collateral — allowing Chislehurst homeowners to access equity at rates of 4.5–7% in 2026, without disturbing their current deal. Combined LTV across both loans typically cannot exceed 75–85% with mainstream lenders (Fox Davidson, January 2026; ResiQuote, April 2026).

When Does a Personal Loan Make Sense for a Chislehurst Extension?

A personal loan is the simplest path to extension financing — no property valuation, no solicitor, no LTV calculation. For smaller projects, it can also be the fastest. The catch is that the maths only work at the lower end of the budget spectrum.

In 2026, personal loan rates run 6–10% for borrowers with good credit history, with the most competitive pricing available on amounts between £7,500–£25,000 (ResiQuote, April 2026). Maximum terms are capped at around 7 years — which means monthly repayments are noticeably higher than mortgage-based routes spread over 20 or 25 years.

As a rough example: £25,000 over 5 years at 7% costs around £495 per month, with total interest of roughly £4,700 over the term. The monthly payment is manageable. The rate isn't ruinous. But for anything above £30,000–£35,000, the comparison with secured borrowing becomes unfavourable quickly.

Where a personal loan does make sense in Chislehurst:

Think of a utility room addition, a small rear lobby, or a modest garden room rather than a full open-plan kitchen extension. If your project runs to £15,000–£22,000 — perhaps because you're working within conservation area constraints that limit the scope of what's permitted — a personal loan is clean, quick, and keeps your property equity entirely separate from the decision.

What it isn't suited for: most full Chislehurst extensions. Single-storey rear extensions in BR7 realistically cost £56,000–£90,000. At those figures, a secured route almost always wins on total cost — even accounting for arrangement fees and legal costs.

Which Finance Route Fits Your Property Type and Street?

The right finance route in Chislehurst depends as much on your specific property, LTV position, and conservation area status as it does on your income or credit score. The table below maps typical scenarios.

📊 Buildaway equity guide — Chislehurst BR7: Based on HM Land Registry data (April–May 2026), here's how much additional financing a typical BR7 homeowner at 75% LTV could access, assuming a 40% LTV outstanding mortgage:

| Property Type | Area / Road | Avg Value | Additional Borrowing at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Edwardian semi-detached | Lower Camden, Watts Lane | £620k–£750k | £155k–£187k | Remortgage or Further Advance |

| Victorian terrace | High Street, Holbrook Lane | £500k–£650k | £125k–£162k | Further Advance or Second Charge |

| 1930s detached | Manor Park Road, Elmstead | £700k–£900k | £175k–£225k | Remortgage (deal ending) or Further Advance |

| Large detached | Beaverwood Road, Old Hill | £850k–£1.1m+ | £212k–£275k+ | Any route; remortgage most flexible |

| Period flat / maisonette | Lubbock Road, Royal Parade | From £360k | From £90k | Personal loan for smaller projects |

\*Assumes 40% LTV outstanding balance; figures indicative only. Always seek independent financial advice.

The conservation area factor — specific to Chislehurst. Chislehurst holds the largest conservation area in the London Borough of Bromley, taking in properties around Camden Place, Royal Parade, St Nicholas Church, and large sections of the residential streets running toward Chislehurst Common. Within these boundaries, all external alterations require specific consent — not just listed buildings. Some lenders treat this as a planning risk and won't release funds until a decision notice has been issued. If your property sits inside the conservation area boundary, start the Bromley Council planning conversation before you speak to any lender.

🔑 Citation capsule: Chislehurst holds the largest conservation area in the London Borough of Bromley, covering significant parts of the BR7 residential area including streets around Camden Place, Royal Parade, and Chislehurst Common (Chislehurst Society, 2025). Many lenders financing extensions within designated conservation areas require full planning approval before releasing funds, as restrictions on materials and design directly affect the viability and value of the property used as security.