Blackheath straddles two postcodes — SE3 across Lewisham and SE10 across Greenwich — and for homeowners on streets like Dartmouth Row, Tranquil Vale, or the Cator Estate, this dual-borough reality shapes everything from planning permission to mortgage lending. In 2026, terraced houses in SE3 average £818,000 and semi-detached homes reach £935,000, making Blackheath one of the most equity-rich addresses in South East London (Rightmove / HM Land Registry, 2026).

A rear extension or wraparound kitchen on a Georgian townhouse or Victorian terrace here can run to £55,000–£120,000 when conservation-area design requirements are factored in. Very few families have that sitting idle. The real question — the one that determines whether your extension gets built this year or sits in a folder for another two — is which finance route costs you least, and which one fits your specific situation.

Related guide: How much a home extension costs in Blackheath

This guide maps every option — remortgage, further advance, second-charge mortgage, and personal loan — to the specific property types across SE3 and SE10. Whether you're in a Victorian terrace near Blackheath Village, a Span house on the Cator Estate, or a Georgian townhouse on Dartmouth Row (SE10), the right answer isn't the same for everyone.

TL;DR:

Blackheath SE3 terraced homes average £818,000 and semis reach £935,000 in 2026 (Rightmove / HM Land Registry). Most SE3 and SE10 homeowners hold substantial equity — often at LTV ratios below 50%. Remortgaging at 5-year fixed rates of 4.25–4.50% is typically the most cost-effective route when your deal is ending. If you're mid-fix or your property sits within the Blackheath Conservation Area, a further advance or second-charge mortgage usually works out smarter. Dual-borough planning (Lewisham vs Greenwich) adds a step some lenders want resolved before releasing funds.

Why Are Blackheath Homeowners Choosing to Extend Rather Than Move?

Blackheath is a market where the properties people want rarely come up — and when they do, competition is fierce. A Georgian townhouse on Eliot Place (SE3) or a detached Victorian on Hervey Road doesn't come to market twice in a decade. Once you're in, the instinct is to make the space work rather than risk losing your position in an area where every sale is contested.

The transaction cost of moving at this price point is severe. Stamp duty on an £850,000 Blackheath property now runs to £32,500 under 2026 HMRC rates. Add estate agent fees of £12,000–£20,000, conveyancing at £3,000–£5,000, and the renovation costs you'll almost certainly face on any period property you buy, and the real cost of moving to gain a room easily exceeds £60,000–£90,000.

That same money directed into your existing home becomes a different calculation entirely. Extensions across South East London return £1.20–£1.50 for every £1 spent, adding 10–20% to property value (RICS, 2025). On an SE3 terraced home worth £818,000, a well-executed rear extension could add £81,800–£163,600 in value — dwarfing the financing cost of the project.

Cormac Hegarty, Director at Buildaway: "Blackheath is one of the most considered markets we work in. The homeowners here have usually been in their property for several years, they know the street values, and they've already done the maths on moving. What they need help with isn't the decision to extend — it's understanding which finance route preserves the most value and fits their mortgage situation."

Around 24% of UK homeowners who seriously considered moving in early 2026 chose to extend instead, citing moving costs and disruption as primary factors (Quick Move Now, Q1 2026). In Blackheath — where Blackheath Station offers 15 minutes to London Bridge and 20 minutes to Charing Cross, and where the heath itself keeps demand consistently high — that preference to stay is even more pronounced.

🔑 Citation capsule: Home extensions in South East London typically return £1.20–£1.50 for every £1 spent and add 10–20% to property value (RICS, 2025). For a Blackheath homeowner with an SE3 terraced property valued at £818,000 in 2026 (Rightmove / HM Land Registry), this translates to £81,800–£163,600 in potential added equity — substantially more than the cost of financing a well-planned rear or side extension.

How Much Does a Home Extension Actually Cost in Blackheath in 2026?

Before approaching any lender, you need a robust budget. Getting this wrong by even £20,000 — a figure easily absorbed by heritage-material requirements in Blackheath's conservation zone — is how homeowners end up on expensive bridging finance with building work half-done.

In London and the South East, single-storey extensions cost £2,800–£4,500 per m² in 2026 — a 20–40% premium over national average build rates (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A 20m² rear extension on a Victorian terrace near Blackheath Village or a semi-detached on Shooters Hill Road (SE3 8UW) realistically totals £60,000–£100,000 once professional fees, building control, and a sensible contingency are included.

Blackheath's conservation area status adds costs that first-time extenders consistently underestimate. Properties on Montpelier Row (SE3), Lawn Terrace (SE3 9LJ), and Dartmouth Row (SE10) — many Grade II listed — may require matching brick, traditional sash windows, and heritage-compliant render, adding 10–20% to a comparable project on an unlisted street. A Heritage Design Statement and pre-application advice from either Lewisham or Greenwich Council (depending on which side of the SE3/SE10 boundary your home sits) typically costs £800–£2,500 before a single brick is laid.

The dual-borough factor. Blackheath's geography means SE3 homeowners apply to the London Borough of Lewisham; those in SE10 apply to the Royal Borough of Greenwich. Design expectations are broadly similar, but the application portals, validation requirements, and decision timescales differ. Budget for pre-application advice from the correct council — and confirm which authority covers your address before approaching any lender, since some require this information upfront.

The underlying approval rate is reassuring: 87% of householder planning applications in England were approved in the year ending September 2025 (DLUHC, Dec 2025) — including in conservation areas where design quality is carefully considered.

Related guide: Single vs Double Storey Extension — Blackheath

🔑 Citation capsule: In London and the South East, single-storey home extensions cost £2,800–£4,500 per m² in 2026 — a 20–40% premium over the national average (getestimateai.co.uk, March 2026; RICS BCIS, 2025). For Blackheath homeowners in the designated conservation area, heritage-compliant materials and design statements add a further 10–20% to total project costs versus comparable non-designated properties in SE3 or SE10.

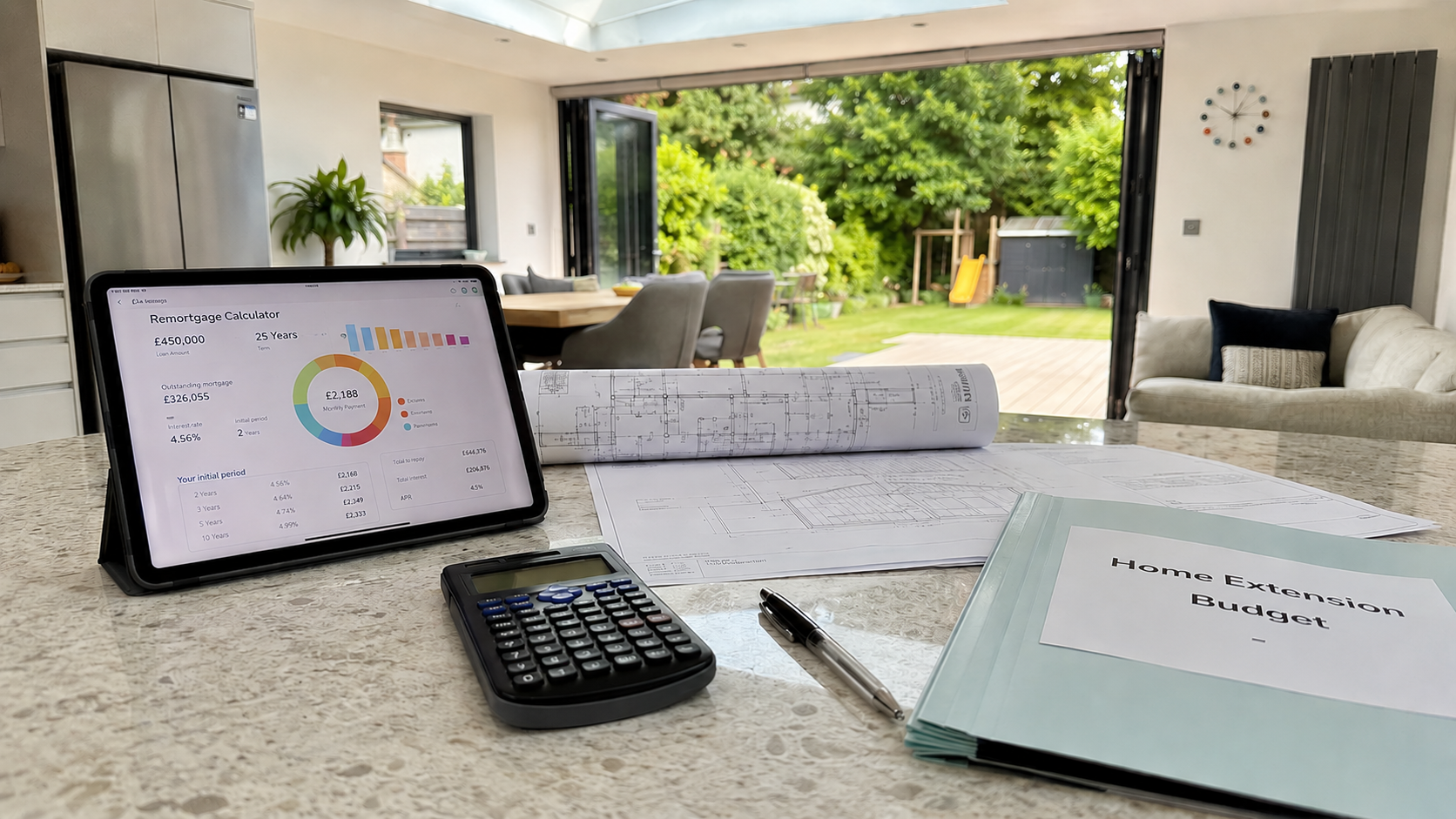

Should You Remortgage to Fund Your Blackheath Home Extension?

Remortgaging is the route most Blackheath homeowners land on — and when the timing lines up with your current deal, it's typically the most cost-effective option available.

The structure is familiar: your existing mortgage is replaced with a new, larger one. The difference between your previous outstanding balance and the new amount is released as cash to fund the build. In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Given that SE3 terraced homes average £818,000 and semi-detached homes approach £935,000 in 2026 (Rightmove / HM Land Registry, 2026), Blackheath homeowners who have been in their property for five or more years frequently hold LTV ratios well below 50% — unlocking the sharpest tier of remortgage pricing.

When does remortgaging make sense for a Blackheath homeowner?

It makes the most sense when your current fixed deal is ending, or has already expired. UK Finance estimates around 1.8 million fixed-rate mortgages will expire in 2026 — many locked in below 2% in 2021. If you're in that group, your deal is ending whether you remortgage or not. Doing it now, and releasing extension cash in the same transaction, is one of the most efficient uses of the remortgage window.

The alternative to acting is drifting onto your lender's Standard Variable Rate (SVR), currently averaging 6.49–7.00% (HomeOwners Alliance, May 2026). For an SE3 homeowner with £350,000 outstanding, the monthly step-up from a 1.8% fix to SVR is material. Remortgaging at 4.25% and releasing £70,000 for a rear kitchen extension can cost only marginally more per month than doing nothing and sitting on SVR — a comparison that surprises almost every homeowner who runs the numbers.

The Early Repayment Charge (ERC) calculation

Mid-deal Blackheath homeowners face a more complex picture. Many fixed at 1.5–2% in 2021 and still carry ERCs of 1–5% on significant outstanding balances. For a £400,000 outstanding mortgage, a 3% ERC means £12,000 in exit costs. If the monthly saving from remortgaging is £400, that ERC doesn't break even for 30 months. In this scenario, a further advance or second-charge mortgage almost always wins.

💡 Our finding: Blackheath's SE3 price growth ran at +3.22% year-on-year to August 2025 (londonhouseprices.co.uk), outpacing the broader London average as supply in this highly desirable corridor remained constrained. For homeowners who've owned for five or more years, equity positions are stronger than the current rate environment might suggest — and that LTV advantage translates directly into better remortgage deals.

The 6-month rule. Most lenders let you lock in a new remortgage rate up to 6 months before your current deal expires — at no cost and with no obligation to switch early. If your fix ends before November 2026, the window to act without an ERC is open now. Remortgaging activity rose 13.7% in 2025 to 1.86 million loans (UK Finance); specialist brokers familiar with Blackheath's dual-borough planning context are worth engaging from the outset.

Related guide: Planning Permission for a Blackheath Home Extension

🔑 Citation capsule: In May 2026, the Bank of England base rate stands at 3.75%, with the best 5-year fixed remortgage deals at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026; Bank of England, May 2026). Blackheath SE3 terraced homes averaging £818,000 in 2026 (Rightmove / HM Land Registry) give long-term owners LTV positions well below 50%, accessing the most competitive remortgage pricing available in the market.

What Is a Further Advance — and Does It Suit Blackheath's Conservation Area Complexity?

A further advance is additional borrowing from your existing mortgage lender, secured against the same property, without breaking your current deal. It's the route most often skipped — and for Blackheath homeowners who fixed at a low rate and don't want to lose it, it can be the smartest option available.

Here's the practical advantage in a conservation area context: a further advance doesn't require your lender to re-underwrite your entire mortgage. Since you're already on their books, the application is simpler, the timeline shorter, and the affordability checks leaner. Some lenders process further advances in 2–4 weeks — considerably faster than a full remortgage, and fast enough to let you commission your architect and start the planning process without waiting for full mortgage completion.

What you should realistically expect:

The rate on a further advance typically sits a notch above your existing mortgage rate — lenders price the additional risk separately. But it's materially cheaper than a personal loan and avoids the ERC a full remortgage would trigger mid-deal. The amounts available are sometimes capped, and not every lender offers the facility, but if yours does, it's worth pricing before anything else.

🏡 Buildaway tip: Homeowners on the Cator Estate (SE3 0TX, SE3 9LA) — where Span houses and Georgian conversions regularly command £700,000–£1,100,000+ — tend to sit at LTV ratios that put them firmly in the prime bracket for further advance applications. The same applies to Victorian terraces near Blackheath Village on streets like Foxwood Road (SE3 9HT) and Glenluce Road (SE3 7SB). Strong security value and an established payment history together make these applications straightforward for most major lenders.

Always confirm a formal decision in principle before committing to your build programme. Good Blackheath extension specialists are in high demand — the right builder won't hold a start date without confirmed finance.

Related guide: How long a home extension takes in Blackheath

Option 3: Secured Loan (Second-Charge Mortgage) — The Case for Blackheath's Listed and Conservation Properties

A second-charge mortgage is a separate loan secured against your home, sitting behind your existing mortgage. It's the tool that solves two very specific Blackheath problems that most generic finance guides don't mention.

Problem one: the pre-planning lender requirement. A number of mainstream high-street lenders require full planning permission before releasing remortgage funds against a Blackheath conservation area property. For Grade II listed homes on Dartmouth Row (SE10 8BF), Montpelier Row, or Eliot Place (SE3), this creates a timing bind: you need finance to commission architectural drawings and structural surveys, but the lender wants planning first. Second-charge lenders typically assess the property on its security value rather than applying a blanket pre-planning condition — removing that bottleneck.

Problem two: the dual-borough complication. SE10 homeowners apply to the Royal Borough of Greenwich; SE3 homeowners go to Lewisham. Some lenders applying tight underwriting to conservation-designated properties require clarity on which planning authority holds jurisdiction and what pre-application guidance says before releasing funds. Second-charge lenders are generally more flexible on this documentation requirement.

Rates in 2026 run 4.5–7% depending on LTV and credit profile (Fox Davidson, Jan 2026; ResiQuote, April 2026). Combined LTV across both loans typically can't exceed 75–85% with mainstream second-charge lenders.

This route suits you if:

- You're mid-fix with a meaningful ERC and a rate below 2.5%

- Your property is within the Blackheath Conservation Area and your preferred lender wants pre-planning sign-off

- You're self-employed or operate through a limited company — specialist second-charge lenders assess income more flexibly

- Your SE10 property involves Grade II listed building consent, adding complexity that makes high-street remortgage underwriting cautious

Your home secures both loans — this matters and shouldn't be minimised. Get independent mortgage advice before committing.

🔑 Citation capsule: A second-charge mortgage allows Blackheath homeowners to borrow against their property equity at 4.5–7% in 2026 without disturbing their existing mortgage deal (Fox Davidson, January 2026; ResiQuote, April 2026). For SE3 and SE10 properties within the Blackheath Conservation Area — where mainstream lenders may require full planning approval before releasing remortgage funds — second-charge lenders typically offer a more flexible pre-planning finance route.

When Does a Personal Loan Make Sense for a Blackheath Extension?

Rarely — but there's a specific band of projects where it's the right answer.

Personal loan rates run 6–10% for borrowers with strong credit profiles in 2026, with the best rates on amounts between £7,500–£25,000 (ResiQuote, April 2026). Repayment terms cap at 7 years — far shorter than any mortgage-based route — which pushes monthly payments higher and makes personal loans expensive for anything above £25,000 in project cost.

The maths: £25,000 over 5 years at 7% costs £495/month and totals £29,700 in repayments — £4,700 in interest. For a modest single-storey utility or garden room addition on an SE3 9 flat or a smaller terrace near Kidbrooke — where project costs might run £16,000–£22,000 — a personal loan is clean, fast, and unsecured. No valuation, no solicitor, no equity at risk.

What a personal loan is definitively not suited for: the larger-scale projects most Blackheath families pursue. A rear kitchen-diner extension on a Victorian terrace near Tranquil Vale, or a side return on an Edwardian semi near Westcombe Park, will realistically cost £70,000–£130,000. At those sums, the rate differential between a personal loan and a remortgage costs tens of thousands in additional interest over the life of the borrowing.

Which Finance Route Fits Your Blackheath Property — by Postcode and Type?

Blackheath's housing stock is genuinely varied — more so than most parts of South East London. You have Grade II listed Georgian townhouses on Dartmouth Row (SE10) and Eliot Place (SE3), Victorian terraces in Westcombe Park (SE3 7) and near All Saints Church, Edwardian semis on Shooters Hill Road (SE3 8), mid-century Span houses on the Cator Estate (SE3 0, SE3 9), and 1930s semis on streets like Weyman Road and Foxwood Road. Each carries a different equity position and a different set of finance considerations.

📊 Buildaway equity calculator — Blackheath postcodes: Based on Rightmove and HM Land Registry data (2026), here's the approximate additional borrowing available at 75% LTV for Blackheath homeowners, assuming a 45% LTV outstanding mortgage:

| Property Type | Area | Approx Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Georgian townhouse (Grade II listed) | SE10 (Dartmouth Row, Vanbrugh Hill) | £700k–£1.1m+ | £206k–£371k | Remortgage or Second Charge (pre-planning flexibility) |

| Victorian terrace | SE3 7 (Westcombe Park, Glenluce Rd) | £700k–£900k | £206k–£281k | Remortgage or Further Advance |

| Edwardian semi-detached | SE3 8 (Shooters Hill Rd, Kidbrooke area) | £600k–£800k | £173k–£248k | Further Advance or Remortgage |

| Span / mid-century (Cator Estate) | SE3 0 / SE3 9 (Cator Estate) | £550k–£900k | £161k–£281k | Second Charge if in conservation zone |

| 1930s semi-detached | SE3 9 (Weyman Rd, Foxwood Rd) | £500k–£750k | £138k–£225k | Further Advance or Remortgage |

| Period flat / conversion | SE3 / SE10 (various) | From £350k | From £75k | Personal loan for compact scope |

*Assumes 45% LTV outstanding; figures indicative only — seek independent mortgage advice.

The dual-borough planning reality — a Blackheath-specific risk. Unlike Bromley or Chislehurst, where a single local authority manages planning, Blackheath homeowners face two separate regimes. If your address puts you in SE10, your planning application goes to Greenwich. If you're in SE3, it goes to Lewisham. Some lenders — particularly those who've encountered delays on Blackheath conservation area applications in the past — apply additional scrutiny before releasing remortgage funds. Clarify your planning authority and get a pre-application response in hand before approaching your lender. It strengthens your application and removes a common source of delay.

Related guide: Planning Permission for a Blackheath Home Extension

🔑 Citation capsule: Blackheath's SE3 and SE10 postcodes span two planning authorities — Lewisham and Greenwich respectively — with the designated Blackheath Conservation Area managed across both boroughs. Terraced homes in SE3 average £818,000 in 2026 and semi-detached properties reach £935,000 (Rightmove / HM Land Registry). Long-term homeowners in Georgian and Victorian stock frequently hold LTV ratios below 45%, giving them access to the most competitive remortgage and further advance rates in the market.