According to HM Land Registry data, the average property in the London Borough of Bexley sold for £519,768 in the year to early 2026 — a figure that places DA5, DA6, and DA7 homeowners among the most equity-secure in outer South East London (HM Land Registry via House Price Finder, 2026). For families squeezed into a 1930s semi near Danson Park, or occupying a period cottage in Old Bexley Village, that number represents a very real lever — one that can fund a serious rear extension without selling up.

The challenge isn't whether you can access that equity. It's knowing which finance route gives you the best outcome for your specific property, deal, and timeline.

Related guide: How much a home extension costs in Bexley

A single-storey rear extension in South East London runs £35,000–£90,000. Very few households hold that as cash. This guide breaks down the full range of options — remortgage, further advance, second-charge mortgage, and personal loan — and maps them against the specific property types and postcodes that define the London Borough of Bexley, from interwar semis in Bexleyheath (DA6) and Welling (DA16) to detached homes around Bexley Village (DA5) and the tree-lined roads of Sidcup (DA14).

TL;DR:

A typical single-storey rear extension in Bexley costs £35,000–£90,000 in 2026. With average property values at £519,768 (HM Land Registry, 2026), most DA5–DA16 homeowners hold enough equity to fund one. Today's 5-year fixed remortgage rates of 4.25–4.50% outperform personal borrowing by a wide margin. Mid-fix on a low rate? A further advance or second-charge mortgage frequently delivers a better result.

Why Are Bexley Homeowners Choosing to Extend Rather Than Move?

The hidden cost of moving is what keeps most Bexley families from going through with it. Stamp duty on a £550,000 home under the 2025 SDLT rules lands at approximately £17,500 (Fox Davidson Stamp Duty Calculator, 2026). Factor in estate agent fees (£9,000–£15,000), conveyancing on both sides (£2,000–£4,000), and removals, and you're looking at £30,000–£38,000 in transaction costs before a single nail goes in.

That's money that creates nothing. An extension of similar or greater cost builds equity instead. Extensions in South East London typically return £1.20–£1.50 for every £1 spent, adding 10–20% to property value (RICS, 2025). On a Bexley home at £519,768, the maths point to £51,977–£103,954 in potential added value.

Walk the planning portal for Bexleyheath or Albany Park and the decision is visible street by street. Rear and side extensions are under construction across the interwar streets that define this borough. Around 24% of UK homeowners who seriously evaluated a move in early 2026 chose to extend instead, with transaction costs and disruption cited as the deciding factors (Quick Move Now, Q1 2026). In Bexley's case, the commuter-friendly transport links — Bexleyheath and Sidcup stations both offering fast routes into central London — reinforce the logic of staying put and gaining space.

Cormac Hegarty, Director at Buildaway: "Bexley homeowners are pragmatic. They've done the stamp duty calculation, they know their street, and they've usually already decided to extend before we meet. What they need from us is an honest view on cost, timeline, and how to structure the finance. That's what this guide delivers."

What makes Bexley particularly interesting from a finance perspective is its internal variation. DA5 (Bexley Village) carries average property values of £571,388 — well above the borough mean — while DA14 (Sidcup) sits closer to £431,000 (Property Investments UK, 2026). The right finance route depends heavily on which end of that spectrum your home sits.

🔑 Citation capsule: Home extensions in South East London typically return £1.20–£1.50 for every £1 spent and add 10–20% to property value, according to RICS (2025). For the average Bexley homeowner at £519,768, this represents £51,977–£103,954 in potential added equity — a meaningful return that in most cases comfortably outpaces financing costs over the life of the project.

What Does a Home Extension Actually Cost in Bexley in 2026?

Arriving at a lender with a vague build estimate is one of the most common mistakes Bexley homeowners make. You need a project total — not a per-square-metre figure pulled from a national guide — because London and the South East carry a significant cost premium.

In 2026, single-storey extensions across the South East London cost band run £2,800–£4,500 per m², compared to a national average of £2,000–£2,800 (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A 20m² rear addition to a DA6 semi-detached — a very common project type for Bexley — realistically runs £56,000–£90,000 when professional fees, building regulations, and a 10% contingency are included.

Bexley's traditional housing stock introduces some specific cost variables. Semi-detached homes that share a flank wall — common across the DA6 and DA7 streets off Bexleyheath and Barnehurst — will almost certainly require a party wall surveyor, budgeted at £1,000–£2,500 per neighbouring property. Householder planning applications cost £206. Building control runs £400–£2,000 depending on project scope. Properties within any of Bexley's 31 designated conservation areas may require a heritage design statement, adding to architect fees.

Bexley's planning department approved 88.4% of householder planning applications in the year to April 2026 (BILTD Planning Guide, April 2026) — a strong success rate that reflects the borough's relatively permissive approach to residential extensions. Even so, knowing your exact project budget before approaching a lender protects you from mid-build shortfalls that push families onto expensive bridging finance.

Related guide: Single vs Double Storey Extension in Bexley

🔑 Citation capsule: In London and the South East, single-storey extensions cost £2,800–£4,500 per m² in 2026 — 20–40% above the national average. A 20m² rear extension on a Bexley semi-detached in DA6 or DA7 therefore runs £56,000–£90,000 in total project cost including professional fees and contingency (RICS BCIS, 2025; getestimateai.co.uk, March 2026).

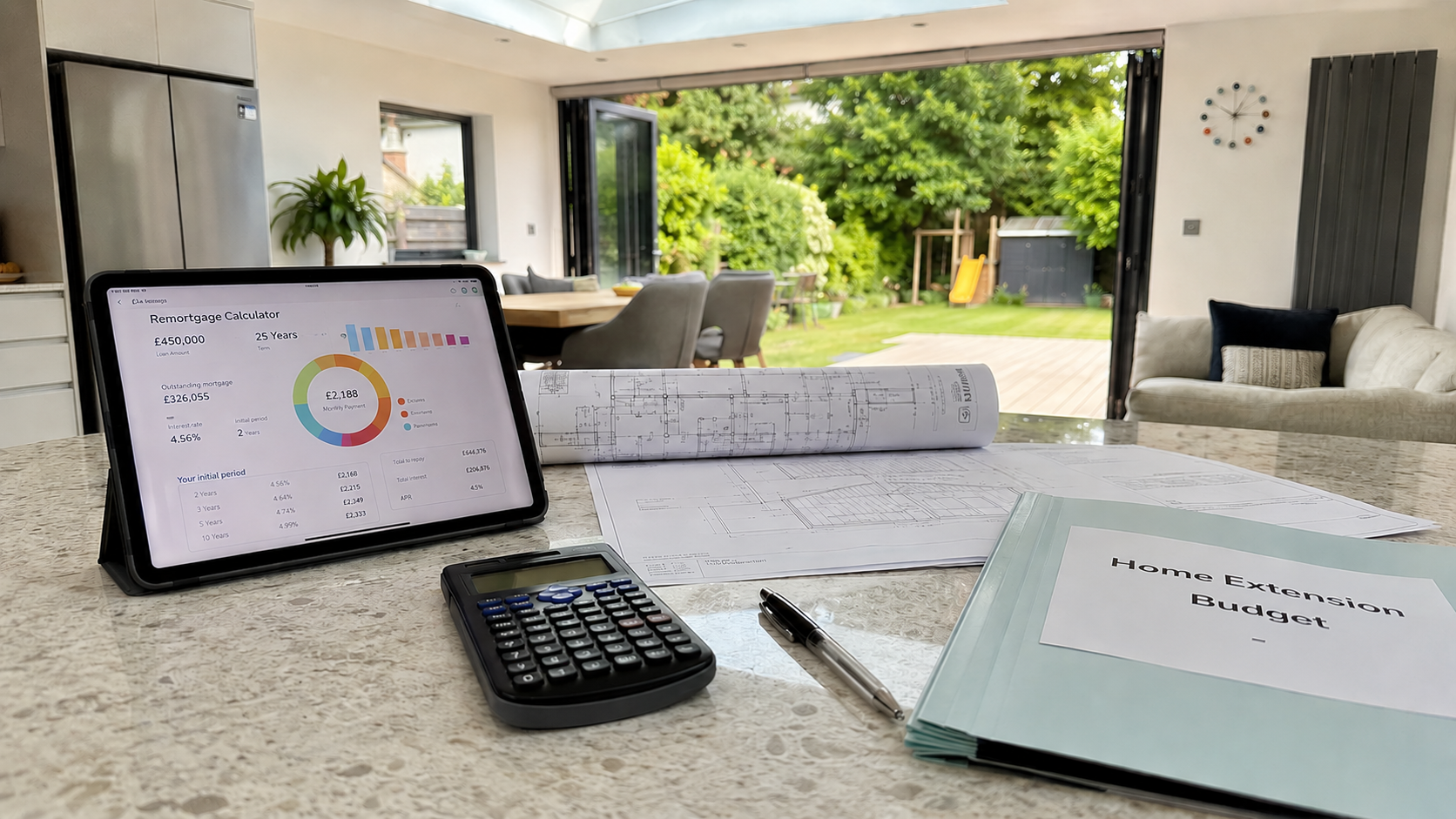

Should You Remortgage to Fund Your Bexley Home Extension?

Remortgaging remains the most widely used finance route for Bexley homeowners planning an extension — and when your timing is right, it's typically the lowest-cost option available.

The process works by replacing your current mortgage with a larger one at a new rate. The additional borrowing above your existing balance is released as cash for the build. In May 2026, competitive 5-year fixed deals sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). At 75% LTV the rate climbs slightly, but still undercuts personal loan and credit card borrowing by a significant margin.

The window that matters is your deal expiry. UK Finance estimates around 1.8 million fixed-rate mortgages will expire in 2026 (UK Finance), many of them originated during the 2021 ultra-low rate environment at below 2%. If yours is among them, your rate is going to change regardless. Acting now means you lock in competitive terms and release extension funding in a single application, rather than going through two separate processes.

The cost of inaction is measurable. A lender's Standard Variable Rate currently averages 6.49–7.00% (HomeOwners Alliance, May 2026). On a £280,000 outstanding mortgage, rolling onto SVR instead of securing a 4.25% deal adds around £1,100 per month. Remortgaging at a competitive rate while releasing £60,000 for an extension can carry almost the same monthly cost as doing nothing.

The ERC problem for mid-deal borrowers. If you fixed in 2021 and still have 12–18 months to run, your Early Repayment Charge needs factoring in carefully. A 2% ERC on a £280,000 balance is £5,600. If a lower rate only saves £180 per month, break-even takes over 30 months. In that scenario, either a further advance or second-charge mortgage will typically produce a better financial outcome.

💡 Our finding: DA5 (Bexley Village) has seen house prices grow 10.8% in the year to May 2026 (HouseMetric, May 2026) — an outlier even by South East London standards. That price growth directly strengthens LTV ratios for DA5 homeowners, putting some of the most competitive remortgage rates within reach for properties that were borderline cases 12 months ago.

The 6-month rule: Lenders allow you to secure a new remortgage rate up to 6 months before your current deal ends, without triggering any ERC or requiring an early exit. If your fixed term expires before November 2026, the application window is open right now.

Remortgaging volumes grew 13.7% in 2025 to 1.86 million loans (UK Finance), reflecting how many households are navigating deal expiry. Brokers are in demand — book early.

Related guide: Planning Permission for a Bexley Home Extension

🔑 Citation capsule: In May 2026, competitive 5-year fixed remortgage deals are available at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). UK Finance estimates 1.8 million fixed-rate mortgages will expire in 2026 — many held by homeowners locked in below 2% in 2021 — making this year the primary window to remortgage and release extension funding simultaneously.

What Is a Further Advance — and Does It Apply to Your Bexley Property?

A further advance is an additional loan from your existing mortgage lender, added on top of your current deal without altering or ending it. It's consistently the most underused option for Bexley homeowners — and for a sizeable portion of people with low-rate fixes still to run, it's the right call.

The reason is straightforward. A 1.85% fix running until 2028 is worth keeping. Remortgaging surrenders it. A further advance means your lender creates a second tranche of lending — secured against the same property, at a current market rate — while your original mortgage continues without disruption. You end up with two separate repayments, but your core borrowing cost stays anchored to that low historic rate.

In practice, you can expect: A rate marginally above your existing mortgage rate but well below anything a personal loan offers. Processing timescales of 2–4 weeks rather than the 4–8 weeks typical of a full remortgage. And a simpler application process, because you're already a known customer with payment history on file.

The limitations are worth knowing. Not every lender offers further advances. Some apply an upper cap on additional borrowing. And if your lender's rate isn't competitive, you're not obliged to use them — a second-charge mortgage (covered next) achieves the same effect without touching your primary deal at all.

🏡 Buildaway tip: Homeowners on Danson Road (DA5 1) — one of Bexley's most sought-after residential roads — saw a sale reach £947,000 in March 2026 (HouseMetric, May 2026). That level of property value typically translates to very low LTV ratios, unlocking the most competitive further advance rates available from mainstream lenders. If your home is in that price bracket, a further advance is usually the first option worth exploring.

Secure a written decision in principle before signing any build contract. Good builders in Bexley have forward order books. Confirmed finance must come before programme commitments, not after.

Related guide: How long a home extension takes in Bexley

Option 3: Secured Loan (Second-Charge Mortgage) — When Does It Work?

A second-charge mortgage is a separate borrowing facility secured against your property, sitting behind your first mortgage in priority order. It gives you access to your equity without forcing any changes to your existing deal — making it particularly valuable for Bexley homeowners locked into terms they don't want to lose.

In 2026, second-charge rates typically range from 4.5–7% based on credit profile and LTV (Fox Davidson, Jan 2026; ResiQuote, April 2026). Those rates sit above the best remortgage deals, but the comparison only holds if you ignore the ERC you'd need to pay to remortgage early. Combined LTV across both loans generally cannot exceed 75–85% with mainstream second-charge lenders.

The scenarios where second-charge lending makes sense in Bexley:

- You're mid-fix with a meaningful ERC and don't want to pay it

- You're self-employed, contracting, or have variable income that high-street remortgage underwriting handles poorly

- You need funds in a shorter timeframe than a full remortgage allows

- Your financial circumstances have shifted since the original mortgage application

Bexley's commuter economy draws a significant proportion of professionals, freelancers, and contractors — workers at financial services firms in Canary Wharf, creative agencies in the City, and consultants who rarely have two identical years of income. Second-charge lenders often underwrite this demographic more flexibly than mainstream banks, and that matters when a standard remortgage keeps getting declined or repriced.

A practical caution: both loans use your home as security. Default on either and both are at risk. That's not a deterrent — it's a reason to ensure your repayment plan is stress-tested before you commit.

🔑 Citation capsule: A second-charge mortgage allows Bexley homeowners to borrow against accumulated property equity at rates of 4.5–7% in 2026, without restructuring or exiting their existing mortgage deal. The loan sits behind the primary mortgage and the combined LTV across both loans typically cannot exceed 75–85% of property value (Fox Davidson, January 2026; ResiQuote, April 2026).

When Does a Personal Loan Work for a Bexley Extension?

Speed and simplicity are the personal loan's core advantages — no equity assessment, no property valuation, no solicitor involvement. For projects at the lower end of the cost range, those advantages are genuinely worth something.

Personal loan rates in 2026 run 6–10% for applicants with strong credit profiles, with the best deals concentrated on loan amounts between £7,500–£25,000 (ResiQuote, April 2026). Repayment periods top out at around 7 years, which pushes monthly payments noticeably higher than the same amount spread over a 20–25 year mortgage.

To make the numbers concrete: £25,000 borrowed over 5 years at 7% costs roughly £495 per month, with total repayments of £29,700 — meaning £4,700 in interest paid. The same sum rolled into a remortgage at 4.25% over 20 years carries a lower monthly payment, though total interest rises due to the extended term.

Where a personal loan makes sense for Bexley homeowners:

A small utility extension or garden room in Welling (DA16) or Erith (DA17) — where build costs might sit between £12,000–£22,000 — is a legitimate candidate. The application takes days, not weeks. There's no equity at stake, and no solicitor delay to manage.

What it isn't built for: most Bexley rear extensions. A 20m² rear addition here runs £56,000–£90,000. At that level, mortgage-secured finance wins on cost in every practical comparison.

Which Finance Route Fits Your Bexley Property — by Postcode?

Property values across the London Borough of Bexley span a wider range than most homeowners realise. DA5 (Bexley Village) averages £571,388; DA14 (Sidcup) sits closer to £431,683 (Property Investments UK, 2026). The right finance route depends on which part of that range you occupy.

📊 Buildaway equity snapshot — Bexley postcodes: Based on HM Land Registry and Property Investments UK data (2026), here's how much additional finance a homeowner at 75% LTV could typically unlock, assuming a 50% LTV outstanding mortgage:

| Property Type | Area | Avg Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Detached/period home | DA5 (Bexley Village, Danson Rd) | £571k–£950k+ | £142k–£237k+ | Remortgage or Further Advance |

| Interwar semi-detached | DA6 (Bexleyheath, Welling Rd) | £460k–£540k | £115k–£135k | Further Advance or Remortgage |

| 1930s semi/terrace | DA7 (Barnehurst, Bexleyheath) | £430k–£520k | £107k–£130k | Second Charge (if mid-fix) |

| Suburban semi-detached | DA15 (Sidcup, Albany Park) | £450k–£560k | £112k–£140k | Remortgage most flexible |

| Smaller terrace/flat | DA16 & DA17 (Welling, Erith) | From £350k | From £87k | Personal loan for smaller projects |

*Assumes 50% LTV outstanding balance; indicative figures only. Always seek independent mortgage advice.

Old Bexley Village (DA5) — a special consideration. The Old Bexley (1971) Conservation Area, along with Bexley's other 30 protected zones, carries planning restrictions that some lenders treat with additional caution. For properties within these designations, certain lenders will require full planning consent before releasing funds — because heritage design conditions affect what can physically be built and therefore influence the property's value as security. If your home sits within any of Bexley's conservation areas, begin your planning conversation with the London Borough of Bexley before approaching any finance provider. Getting that sequence right can save months.

🔑 Citation capsule: The optimal financing route for a Bexley home extension varies substantially by postcode. Properties in DA5 — where average values reach £571,388 and recent sales on Danson Road have exceeded £940,000 (HM Land Registry / HouseMetric, May 2026) — typically carry the lowest LTV ratios and access the most competitive further advance and remortgage rates in the borough. Properties within Bexley's 31 conservation areas often require planning approval before lenders will release funds.