In early 2026, the average house price in Beckenham hit £597,000 — and for homeowners across BR3, that figure is more than just a number on a Rightmove page. It represents a substantial pool of equity sitting in the walls of Victorian terraces around Beckenham Junction, Edwardian houses along Foxgrove Road and The Drive, and 1930s semis off Hayes Lane — waiting to fund the open-plan kitchen, the extra bedroom, or the rear extension the family has been talking about for years (HM Land Registry / Rightmove, March 2026).

A single-storey extension across South East London now costs £35,000–£90,000 all in. Few families keep that sitting in a current account. The question, then, is not whether you can afford to extend — it is which finance route gets you there at the lowest overall cost.

Related guide: How much a home extension costs in Beckenham

This guide breaks down every option — remortgage, further advance, second-charge mortgage, and personal loan. Crucially, it maps each one to the actual property types and street values found across Beckenham BR3, from terraces near Beckenham Junction through to conservation-area detacheds around Park Langley.

TL;DR:

A single-storey extension in Beckenham costs £35,000–£90,000 in 2026. With average house prices at £597,000 (HM Land Registry, March 2026), most BR3 homeowners hold enough equity to fund one outright. Remortgaging at today's 5-year fixed rates of 4.25–4.50% beats a personal loan by thousands on any project above £30,000. If you're locked into a below-market rate, a further advance or second-charge mortgage often works out cheaper still.

Why Are Beckenham Homeowners Choosing to Extend Rather Than Move?

Moving in 2026 is an expensive undertaking — and the numbers have swung firmly in favour of extending. Stamp duty on a £700,000 Beckenham property comes to £22,500. Factor in estate agent fees (£9,000–£14,000), conveyancing (£2,000–£4,000), and removals, and you're burning through £35,000–£43,000 before a single box has been unpacked in the new place.

An extension of comparable cost doesn't just spend money — it creates it. Extensions across South East London typically return £1.20–£1.50 for every £1 spent, adding 10–20% to property value (RICS, 2025). On a £597,000 Beckenham home, that range translates to £59,700–£119,400 in added equity.

The sentiment shift is measurable too. Around 24% of UK homeowners who actively considered moving in early 2026 chose to extend instead, with moving costs and disruption named as the deciding factors (Quick Move Now, Q1 2026). Walk the streets behind Kelsey Park or along Wickham Road in BR3 and the rear extension activity on Bromley Council's planning portal tells exactly the same story.

Cormac Hegarty, Director at Buildaway: "Beckenham homeowners are switched on to the maths. They know a bigger house nearby is probably going to cost them £150,000 more plus moving costs, and that an extension achieves most of the same outcome for a fraction of that outlay. The finance question comes up early — and it should."

Beckenham's market has also been sending mixed signals worth paying attention to. Semi-detached houses here averaged £793,028 in recent transactions, and detacheds crossed £1.1 million (KFH Sold Data, 2025). Even in a softening market, that equity base gives most BR3 homeowners significantly more headroom than they realise.

🔑 Citation capsule: A well-executed home extension in South East London typically returns £1.20–£1.50 for every £1 spent and adds 10–20% to property value, according to the Royal Institution of Chartered Surveyors (RICS, 2025). For the average Beckenham homeowner at £597,000, this translates to £59,700–£119,400 in added equity — comfortably ahead of financing costs on any well-planned project.

How Much Does a Home Extension Actually Cost in Beckenham in 2026?

Get the budget right before you approach a lender. Costs in London and the South East consistently run 20–40% above the national average — and BR3 is no exception.

In 2026, single-storey extensions here cost £2,800–£4,500 per m², compared to a UK national average of £2,000–£2,800 (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A typical 20m² rear extension on a BR3 semi — the most common brief we see from Beckenham homeowners — realistically lands between £56,000–£90,000 once professional fees, building control, and a sensible contingency are included.

Hidden costs trip up more Beckenham homeowners than any other single factor. Victorian and Edwardian terraces along Foxgrove Road and The Drive will almost always trigger a party wall obligation — budget £1,000–£2,500 per neighbour. Planning fees for a householder application are £206. Building control charges run £400–£2,000 depending on scope. Properties within the Park Langley Conservation Area carry an additional layer of heritage design scrutiny, which typically adds to architect fees and can lengthen the pre-application process.

The overall picture on approvals is encouraging: 87% of householder planning applications in England were granted in the year ending September 2025 (DLUHC Planning Statistics, Dec 2025). Well-prepared applications in BR3 rarely get refused.

Underestimating your total budget before speaking to a lender is the single most common mistake. A £15,000 mid-build shortfall is how sensible homeowners end up in conversations about bridging finance they never planned for.

Related guide: Single vs Double Storey Extension Guide

🔑 Citation capsule: In London and the South East, single-storey home extensions cost £2,800–£4,500 per m² in 2026 — 20–40% above the UK national average. A typical 20m² rear extension in Beckenham therefore runs £56,000–£90,000 in total project cost, including professional fees and contingency (RICS BCIS, 2025; getestimateai.co.uk, March 2026).

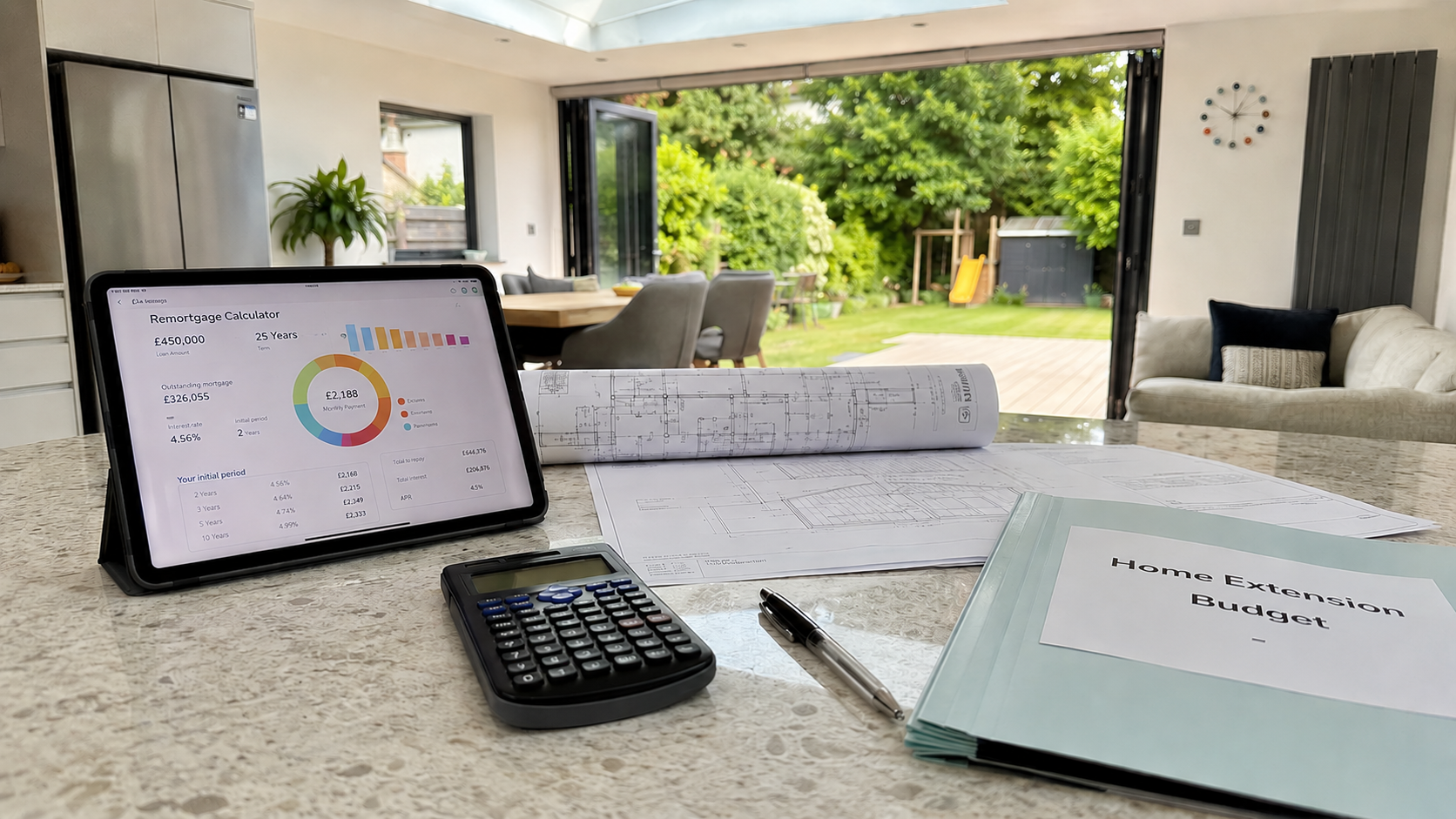

Should You Remortgage to Fund Your Beckenham Home Extension?

Remortgaging is how most BR3 homeowners access extension finance — and with the right timing, it is consistently the lowest-cost route available.

Here is how it works: your existing mortgage is replaced with a new, larger one. The extra amount released above your old balance goes directly towards funding the build. In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). At 75% LTV, rates are still materially cheaper than borrowing unsecured.

When is remortgaging the right call?

It is most powerful when your current fixed-rate deal is ending or has already expired. UK Finance estimates 1.8 million fixed-rate mortgages will expire in 2026 — a large proportion locked in below 2% in 2021. If yours is among them, the deal is ending regardless. Remortgaging to a new rate while releasing extension funds simultaneously avoids two separate application processes and two sets of fees.

Sitting on your hands after a deal expires is genuinely costly. Your lender moves you onto their Standard Variable Rate (SVR), currently averaging 6.49–7.00% (HomeOwners Alliance, May 2026). On a £280,000 outstanding balance, that shift from 1.8% adds close to £1,400 per month. Remortgaging at 4.25% and simultaneously releasing £65,000 for an extension can produce a monthly payment only marginally above drifting onto SVR and doing nothing.

The Early Repayment Charge trap

If you are still mid-deal, the ERC calculation is essential. Homeowners who fixed at 1.5–2% in 2021 often face ERCs of 1–5% of their outstanding loan. A £5,000 ERC to exit a deal that saves £180 a month in interest takes 28 months to break even. In those cases, a further advance or second-charge mortgage is almost always the sharper financial move.

💡 Our finding: Beckenham semi-detacheds averaged £793,028 in 2025, with Wickham Road semis reaching £865,000 (KFH Sold Data; Rightmove Sold Prices Wickham Rd, 2026). That means many BR3 homeowners with modest outstanding mortgages are sitting at LTV ratios of 35–50% — which unlocks the very best remortgage rates on the market and, in some cases, releases more borrowing capacity than the extension itself costs.

The 6-month rule: Most lenders let you lock in a new remortgage rate up to 6 months before your current deal expires — at no ERC and with no obligation to complete early. If your fix ends before November 2026, the time to start the application is now.

Remortgaging activity grew 13.7% in 2025 to 1.86 million loans, per UK Finance. The market is busy. Use a broker — their fee pays for itself in rate comparison alone.

Related guide: Planning Permission for a Beckenham Home Extension

🔑 Citation capsule: In May 2026, the Bank of England base rate stands at 3.75%, with competitive 5-year fixed remortgage deals available at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026; Bank of England, May 2026). UK Finance estimates 1.8 million fixed-rate mortgages will expire in 2026, many locked in below 2% — making this the primary window for Beckenham homeowners to remortgage and fund an extension.

What Is a Further Advance — and Is It the Right Move for You?

A further advance is additional borrowing from your existing mortgage lender, secured against the same property, without exiting your current deal. It is frequently the most overlooked option — and for a meaningful slice of Beckenham homeowners, it is the single best route on the table.

The reason comes down to rate preservation. Suppose you are on a 1.9% fix until late 2027. Remortgaging costs you that rate — full stop. A further advance leaves your current mortgage entirely intact. Your lender simply adds a second loan tranche at today's market rate, charged only on the additional amount. Your existing repayments continue unchanged.

What the process looks like:

The rate applied to a further advance will be slightly above your existing mortgage — but it remains well below unsecured borrowing. Processing times are shorter than a full remortgage: many lenders confirm a further advance in two to four weeks, since the property valuation and income checks are lighter when you are already an established customer.

The limitation to know about upfront: not every lender offers further advances, and some place a ceiling on the additional amount they will lend. If yours does not offer the product, or if their rate is not competitive, a second-charge mortgage achieves the same outcome without requiring you to exit your main deal.

🏡 Buildaway tip: Homeowners on streets like Rectory Road, Southend Road, and The Drive in Beckenham are seeing some of the strongest LTV positions in South East London, with Edwardian properties on these roads regularly transacting at £700,000–£850,000+ (Rightmove Sold Prices Beckenham, 2026). A strong equity position from high property values translates directly into lower LTV ratios — and the most competitive further advance rates from mainstream lenders.

Get a written decision in principle before you commit to a build timeline. The best extension builders in Beckenham carry significant forward books — confirmed finance needs to come before the contract is signed.

Related guide: How long a home extension takes in Beckenham

Option 3: Secured Loan (Second-Charge Mortgage) — When It Makes Sense

A second-charge mortgage is a separate loan secured against your property, ranking behind your first mortgage in order of priority but drawing on the same asset as collateral. It solves a specific problem: accessing your equity without touching a mortgage deal you would be penalised to leave.

Rates in 2026 typically land between 4.5–7% depending on LTV and personal credit profile (Fox Davidson, Jan 2026; ResiQuote, April 2026). That is higher than the best remortgage deals currently on offer. The payoff is straightforward: your existing mortgage is untouched, your low fixed rate is preserved, and you access the equity you need without an ERC.

Second-charge makes practical sense when:

- You have a meaningful ERC on a low-rate deal that has years left to run

- You are self-employed, a contractor, or have variable income, and specialist lenders take a more flexible view of affordability than your current mortgage lender would on a remortgage application

- You need funding released faster than a full remortgage process allows

- Your financial circumstances have shifted materially since you first took out your mortgage

Beckenham's population includes a high proportion of finance professionals, barristers, and contractors who commute into the City or Canary Wharf. For those on complex income structures, second-charge lenders often accommodate income types that high-street remortgage underwriting handles poorly.

One point worth stating plainly: your home is collateral on both loans simultaneously. If either becomes unserviceable, both are at risk. That is not a reason to avoid the route — it is a reason to model your monthly obligations carefully with a broker before committing.

🔑 Citation capsule: A second-charge mortgage — also called a secured loan — sits behind your existing mortgage and allows Beckenham homeowners to borrow against property equity at rates of 4.5–7% in 2026, without altering their current mortgage deal or triggering Early Repayment Charges. Combined LTV across both loans typically cannot exceed 75–85% (Fox Davidson, January 2026; ResiQuote, April 2026).

When Does a Personal Loan Make Sense for a Beckenham Extension?

A personal loan is the most administratively simple route to extension finance — no property valuation, no solicitors, no equity calculation. The limitation is cost, and it shows quickly once the project budget climbs above £25,000.

In 2026, personal loan rates run 6–10% for borrowers with strong credit profiles, with the most competitive rates available on amounts of £7,500–£25,000 (ResiQuote, April 2026). Repayment terms cap out at 7 years, producing monthly payments that are significantly higher than any mortgage-based route spread over 20 years.

The maths to run: £25,000 over 5 years at 7% costs around £495 per month, producing total repayments of £29,700 and £4,700 in interest. Put that same amount on a remortgage at 4.25% over 20 years and the monthly cost drops sharply — though total interest increases over the extended term. For larger sums, the monthly payment gap widens considerably.

When a personal loan is the right call for a Beckenham homeowner:

For a compact utility extension or a side-passage infill on a BR3 terrace with a £15,000–£20,000 budget, the simplicity and speed of a personal loan can genuinely make sense. It is also worth considering when you want to ring-fence your property equity entirely from the renovation decision — for example, if you are close to a remortgage deal expiry and want to keep your options clean.

What it does not suit: the overwhelming majority of Beckenham extensions. Single-storey rear extensions here run £56,000–£90,000. At that scale, a secured route almost always produces a materially lower overall cost.

Which Finance Route Fits Your Beckenham Property — by Street and Postcode?

Generic finance guides stop short of this section. The right route for your project depends heavily on which part of Beckenham you are in and what kind of property you own — because both factors drive your equity position and your access to specific products.

📊 Buildaway equity calculator — Beckenham BR3: Based on HM Land Registry transaction data (March–May 2026), here is how much additional financing a homeowner at 75% LTV could typically unlock, assuming a 50% LTV outstanding mortgage:

| Property Type | Area | Avg Value | Equity at 75% LTV* | Best Finance Route |

|---|---|---|---|---|

| Victorian terrace | BR3 1 (Central Beckenham, Foxgrove Rd) | £550k–£750k | £137k–£187k | Remortgage or Further Advance |

| 1930s semi-detached | BR3 2/4 (Hayes Lane, Blakeney Rd) | £520k–£680k | £130k–£170k | Further Advance or Remortgage |

| Edwardian family house | BR3 3 (The Drive, Rectory Rd) | £650k–£900k | £162k–£225k | Second Charge (if mid-fix) |

| Detached / conservation | BR3 5 (Park Langley, Copers Cope) | £800k–£1.1m+ | £200k–£275k | Any route; remortgage most flexible |

| Flat / smaller terrace | BR3 6 (Beckenham Junction area) | From £313k | From £78k | Personal loan for smaller projects |

*Assumes 50% LTV outstanding balance; figures indicative only. Always seek independent mortgage advice.

Park Langley and Beckenham Place Park — a special category. Properties in and around the Park Langley Conservation Area and near the Beckenham Place Park boundary regularly command £800,000–£1.1 million+, giving homeowners here significantly more equity headroom than elsewhere in BR3. The trade-off: lenders periodically require full planning approval before releasing funds on conservation area properties, because design restrictions from Bromley Council can materially affect a build's viability as collateral. If your property falls within or adjacent to a designated conservation area, start the planning pre-application process with Bromley Council's Development Management team before approaching your lender.

🔑 Citation capsule: The optimal financing route for a Beckenham home extension depends significantly on property type and postcode sector. Homeowners in the Park Langley area of BR3 5 — where detacheds regularly exceed £800,000–£1.1 million (HM Land Registry / Rightmove, 2026) — hold the deepest equity positions in the borough and qualify for the most competitive remortgage and further advance rates. Conservation area properties may require planning approval before lenders will release funds.