Pull back the terrace frontages on any of SW11's most sought-after streets — Brynmaer Road, Sisters Avenue, the roads running off Northcote Road — and you'll find families grappling with the same problem. The houses are beautiful. The gardens are short. The kitchens feel smaller every year. And the average Battersea property now costs £715,000 (ONS / HM Land Registry, Q1 2026).

Moving up the ladder from here doesn't come cheap. It means paying stamp duty, agent fees, and solicitor bills on a transaction worth six or seven figures — and often landing somewhere with a smaller garden and a longer commute. For most Battersea families, the maths of moving have stopped making sense.

This guide covers every realistic finance option for SW8 and SW11 homeowners: remortgage, further advance, second-charge mortgage, and personal loan. It maps each route to the specific property types — and postcodes — where it actually works.

Related guide: How much a home extension costs in Battersea

TL;DR:

A single-storey extension in Battersea costs £35,000–£90,000 in 2026; loft conversions run £45,000–£80,000. With average SW11 house prices at £715,000 (ONS, Q1 2026), most homeowners hold enough equity to fund one. Remortgaging at today's 5-year fixed rates of 4.25–4.50% typically beats a personal loan by thousands. Mid-deal on a low rate? A further advance or second-charge mortgage often works out cheaper still.

Why Are Battersea Homeowners Choosing to Extend Instead of Moving?

Moving in Battersea is expensive in ways that catch people off guard. Stamp duty on an £850,000 SW11 property reaches £33,750. Layer on estate agent fees (£12,750–£21,250), conveyancing (£3,000–£5,000), and London removal charges, and a typical transaction costs £51,500–£65,000 before you've unpacked a single box.

An extension costs a comparable sum upfront — but it adds value rather than burning it. In inner London, well-executed extensions typically return £1.20–£1.50 for every £1 spent, adding 10–20% to property value (RICS, 2025). On a £715,000 Battersea home, that's £71,500–£143,000 in added equity. Against a £33,750 stamp duty bill just to move, the case for extending is difficult to argue with.

There's a local dimension too. SW11 4 — the stretch centred on Northcote Road — has built its reputation as one of London's great family postcodes precisely because its residents chose to invest in their existing homes rather than chase space elsewhere. The "Nappy Valley" identity isn't accidental. It reflects decades of families extending kitchens, adding bedrooms, and converting loft spaces rather than trading the area for somewhere cheaper and larger.

Around 24% of UK homeowners who seriously considered moving in early 2026 opted to extend instead, citing transaction costs and disruption as deciding factors (Quick Move Now, Q1 2026). In Battersea, where transaction values are higher and moving costs correspondingly larger, that proportion almost certainly runs higher.

Cormac Hegarty, Director at Buildaway: "In Battersea, the conversation barely touches on whether to extend. It's always — how do we pay for it, and when can we start? The decision gets made the first time someone runs the stamp duty numbers."

Battersea property values held firm in the year to Q1 2026, rising 1.4% year-on-year while broader inner London values fell 2.3% over the same period (ONS, Q1 2026). The equity built over the past decade is holding. It's available to fund the projects most SW11 homeowners have already decided they want.

🔑 Citation capsule: Moving from an average SW11 property in 2026 generates transaction costs of £51,500–£65,000 in stamp duty, agent fees, and legal costs alone — before any price uplift at the destination. By contrast, a well-executed extension typically returns £1.20–£1.50 for every £1 spent (RICS, 2025), adding £71,500–£143,000 in equity on a £715,000 Battersea home. The financial argument for extending rather than moving has rarely been stronger in this postcode.

What Does a Home Extension Cost in Battersea in 2026?

Setting a realistic budget is the most important step before approaching any lender. An underestimate creates a funding gap mid-project — and bridging finance to plug that gap is expensive.

In 2026, single-storey extensions across London and the South East cost £2,800–£4,500 per m², running 20–40% above the UK national average (getestimateai.co.uk, March 2026; RICS BCIS, 2025). A 20m² rear extension on a typical SW11 terrace runs £56,000–£90,000 in total project cost once you include professional fees, building control, and a 10–15% contingency.

Loft conversions deserve a mention here specifically. Victorian terraces dominate Battersea's housing stock, and many have rear gardens too short to make a meaningful ground-floor extension viable — particularly on mid-terrace properties. A dormer loft conversion adds 30–40m² of additional floor space and costs £45,000–£80,000 without touching the garden at all. Lenders treat them identically to rear extensions for finance purposes.

Party walls are almost universal in SW11. Victorian terrace streets mean shared walls on both sides — budget £1,000–£2,500 per neighbouring property for a party wall surveyor. On a mid-terrace property along a Battersea street, this adds £3,000–£5,000 to your project cost before building work begins. Properties in Battersea's designated conservation areas — particularly near Battersea Park and the streets approaching Albert Bridge — may face additional heritage design requirements that push architect fees higher and extend your pre-application timeline.

The planning picture is generally positive: 87% of householder planning applications in England were granted in the year ending September 2025 (DLUHC, Dec 2025). Getting refused in Wandsworth isn't common, but the borough has specific local requirements. A good architect familiar with SW11 pays for themselves in time saved.

Underestimating your total project cost by even £10,000 mid-build creates real problems. It's the scenario most likely to push a homeowner toward expensive emergency borrowing.

Related guide: Single vs Double Storey Extensions in Battersea

🔑 Citation capsule: In London and the South East, single-storey home extensions cost £2,800–£4,500 per m² in 2026 — 20–40% above the UK national average. A typical 20m² rear extension in Battersea therefore runs £56,000–£90,000 in total project cost including professional fees and contingency. Loft conversions — particularly suited to SW11's Victorian terrace stock where garden depth is limited — run £45,000–£80,000 for a dormer without affecting outdoor space (RICS BCIS, 2025; getestimateai.co.uk, March 2026).

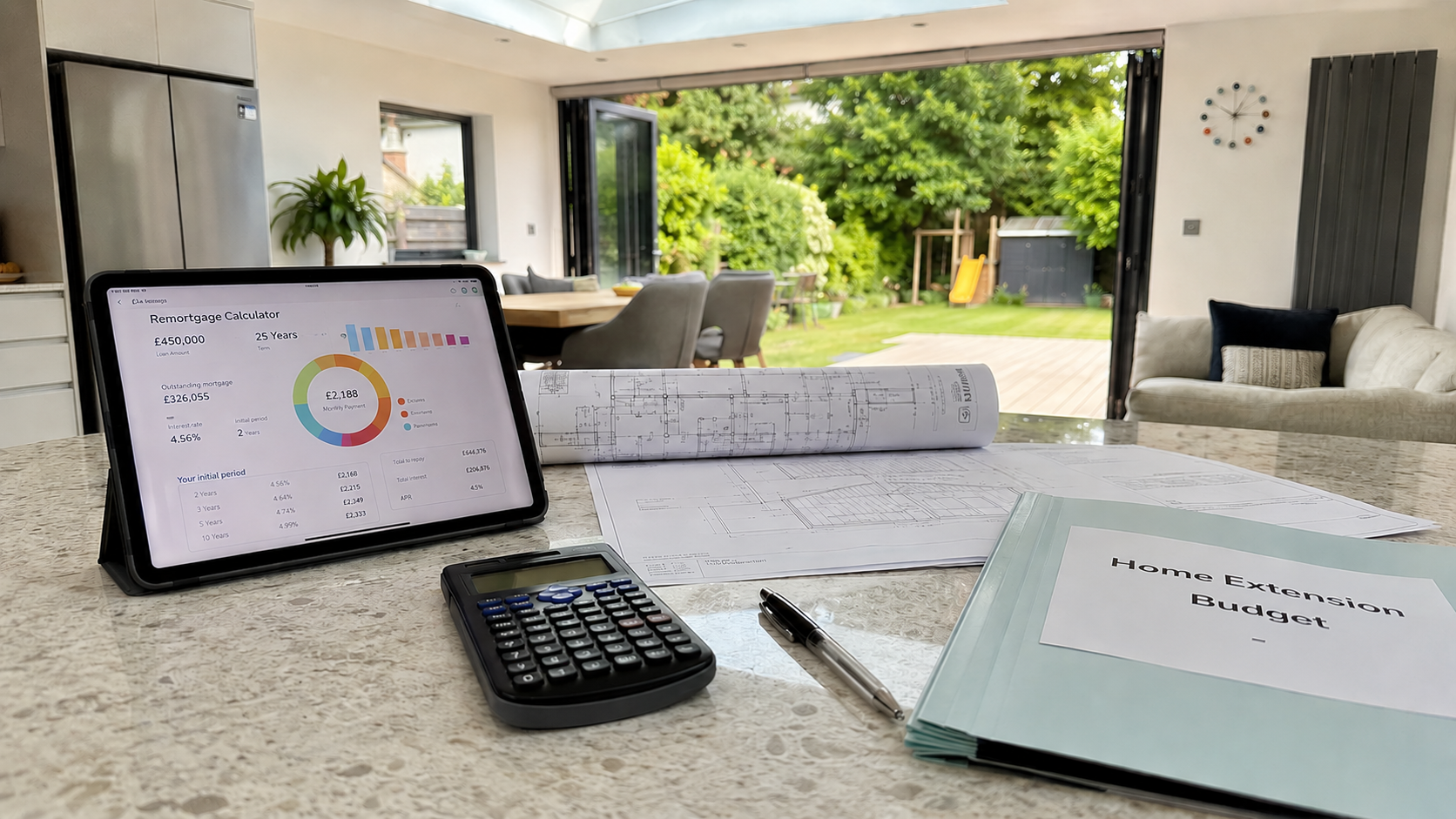

Is Remortgaging the Right Way to Fund a Battersea Home Extension?

Remortgaging is the most common route to extension finance — and when the timing lines up, it's typically the most cost-effective by some margin. The mechanics: replace your current mortgage with a larger one, releasing the difference as a lump sum to fund the build.

In May 2026, competitive 5-year fixed rates sit at 4.25–4.50% at 60% LTV (MoneyfactsCompare, April 2026). Even at 75% LTV — common for homeowners who bought into SW11 at lower valuations — secured borrowing costs remain materially below personal loan rates. The gap widens considerably for amounts above £50,000.

The window that matters most: Around 1.8 million fixed-rate mortgages expire across the UK in 2026, the majority locked in below 2% in 2021 (UK Finance). If your deal ends this year, you're already facing a rate change. Doing nothing puts you on your lender's Standard Variable Rate, currently averaging 6.49–7.00% (HomeOwners Alliance, May 2026). For a £350,000 outstanding balance, the jump from 1.8% to SVR adds over £1,700 per month. Remortgaging at 4.25% and releasing £70,000 for an extension can cost almost the same monthly payment — with a new kitchen, bedroom, or loft to show for it.

Working out your additional borrowing: Most lenders require you to retain 25% equity after borrowing, setting the ceiling at 75% LTV. On an average SW11 property worth £715,000 with £300,000 still outstanding, that's up to £236,250 in additional borrowing — comfortably covering most rear extensions or full loft conversions in the Battersea market.

The Early Repayment Charge trap: If you're mid-deal on a sub-2% fix with a meaningful ERC still running, a straight remortgage rarely stacks up. A £7,500 ERC to switch to 4.25% doesn't break even for nearly three years on a typical SW11 balance. A further advance or second-charge mortgage usually wins in this scenario — and keeps your existing rate intact.

The 6-month rule: You can lock in a new remortgage rate up to 6 months before your current deal expires — no ERC, no obligation to complete early. If your fix ends before December 2026, the right time to apply is now.

💡 Our finding: Battersea's property market is holding firm where many inner London submarkets are softening — values rose 1.4% year-on-year to Q1 2026 while the broader inner London average fell 2.3% (ONS, Q1 2026). This stability means SW11 homeowners are sitting on more usable equity than equivalent mortgagors in softer parts of the capital, and accessing better LTV-based rates as a result.

Related guide: Planning Permission for a Battersea Home Extension

🔑 Citation capsule: Competitive 5-year fixed remortgage rates stood at 4.25–4.50% at 60% LTV in May 2026 (MoneyfactsCompare, April 2026; Bank of England, May 2026). With average SW11 house prices at £715,000 (ONS, Q1 2026) and many homeowners retaining strong equity positions, additional borrowing of up to £236,250 is achievable at 75% LTV — well within range for most Battersea extension and loft conversion projects. UK Finance estimates 1.8 million fixed-rate deals expire in 2026, making this the primary remortgage window.